{kind=link}

Even because the Smokehouse Creek Fire – the biggest wildfire ever to burn throughout Texas – was declared “nearly contained” this week, the Texas A&M Service warned that circumstances are such that the remaining blazes might unfold and much more would possibly get away.

“Today, the fire environment will support the potential for multiple, high impact, large wildfires that are highly resistant to control” within the Texas Panhandle, the service stated.

This 12 months’s historic Texas fires – just like the state’s 2021 anomalous winter storms, California’s latest flooding after years of drought, and a surge in insured losses as a result of extreme convective storms throughout the United States – underscore the variability of climate-related perils and the necessity for insurers to have the ability to adapt their underwriting and pricing to replicate this dynamic atmosphere. It additionally highlights the significance of utilizing superior knowledge capabilities to assist danger managers higher perceive the sources and behaviors of those occasions with the intention to predict and stop losses.

For instance, Whisker Labs – an organization whose superior sensor community helps monitor dwelling fireplace perils, in addition to monitoring faults within the U.S. energy grid – recorded about 50 such faults in Texas forward of the Smokehouse Creek fires.

Bob Marshall, Whisker Labs founder and chief government, instructed the Wall Street Journal that proof suggests Xcel Energy’s gear was not sturdy sufficient to resist the sort of excessive climate the nation and world more and more face. Xcel – a significant utility with operations in Texas and different states — has acknowledged that its energy strains and gear “appear to have been involved in an ignition of the Smokehouse Creek fire.”

“We know from many recent wildfires that the consequences of poor grid resilience can be catastrophic,” stated Marshall, noting that his firm’s sensor community recorded comparable malfunctions in Maui earlier than final 12 months’s lethal blaze that ripped throughout the city of Lahaina.

Role of presidency

Government has a crucial function to play in addressing the danger disaster. Modernizing constructing and land-use codes; revising statutes that facilitate fraud and authorized system abuse that drive up declare prices; investing in infrastructure to scale back pricey harm associated to storms – these and different avenues exist for state and federal authorities to assist catastrophe mitigation and resilience.

Too typically, nonetheless, the general public dialogue frames the present state of affairs as an “insurance crisis” – complicated trigger with impact. Legislators, spurred by calls from their constituents for decrease premiums, typically suggest measures that will are likely to worsen the issue as a result of they fail to replicate the significance of precisely valuing danger when pricing protection.

The federal “reinsurance” proposal put forth in January by U.S. Rep. Adam Schiff of California is a working example. If enacted, it will dismantle the National Flood Insurance Program (NFIP) and create a “catastrophic property loss reinsurance program” that, amongst different issues, would set protection thresholds and dictate score components primarily based on enter from a board through which the insurance coverage business is just nominally represented.

U.S. Rep. Maxine Waters (additionally of California) has proposed a Wildfire Insurance Coverage Study Act to analysis points round insurance coverage availability and affordability in wildfire-prone communities. During House Financial Services Committee deliberations, Waters in contrast present challenges in these communities to circumstances associated to flood danger that led to the institution of NFIP in 1968. She stated there’s a precedent for the federal authorities to step in when there’s a “private market failure.”

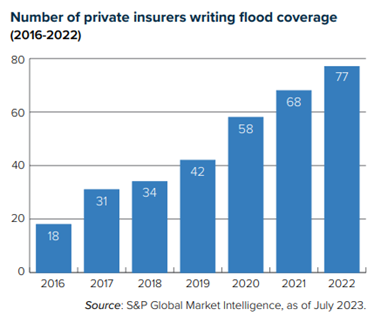

However, flood danger in 1968 and wildfire danger in 2024 couldn’t be extra totally different. Before FEMA established the NFIP, non-public insurers had been usually unwilling to underwrite flood danger as a result of the peril was thought of too unpredictable. The rise of refined laptop modeling has since given non-public insurers a lot better confidence masking flood (see chart).

In California, some insurers have begun rethinking their urge for food for writing householders insurance coverage – not as a result of wildfire losses make properties within the state uninsurable however as a result of coverage and regulatory selections remodeled 30 years in the past have made it exhausting to jot down the protection profitably. Specifically, Proposition 103 and its regulatory implementation have blocked the usage of modeling to tell underwriting and pricing and restricted insurers’ capacity to include reinsurance prices into their premium pricing.

California’s Insurance Commissioner Ricardo Lara final 12 months introduced a Sustainable Insurance Strategy for the state that features permitting insurers to make use of forward-looking danger fashions that prioritize wildfire security and mitigation and embrace reinsurance prices into their pricing. It is affordable to anticipate that Lara’s modernization plan will result in insurers growing their enterprise within the state.

It’s comprehensible that California legislators are desirous to act on local weather danger, given their lengthy historical past with drought, fireplace, landslides and newer expertise with flooding as a result of “atmospheric rivers.” But it’s essential that any such measures be effectively thought out and never exacerbate present issues.

Partners in resilience

Insurers have been addressing climate-related dangers for many years, utilizing superior knowledge and analytical instruments to tell underwriting and pricing to make sure adequate funds exist to pay claims. They even have a pure stake in predicting and stopping losses, reasonably than simply persevering with to evaluate and pay for mounting claims.

As such, they’re perfect companions for companies, communities, governments, and nonprofits – anybody with a stake in local weather danger and resilience. Triple-I is engaged in quite a few tasks aimed toward uniting numerous events on this effort. If you characterize a company that’s working to handle the danger disaster and your efforts would profit from involvement with the insurance coverage business, we’d love to listen to from you. Please contact us with a quick description of your work and the way the insurance coverage business would possibly assist.

Learn More:

Triple-I “State of the Risk” Issues Brief: Wildfire

Triple-I “State of the Risk” Issues Brief: Flood

Triple-I “Trends and Insights” Issues Brief: California’s Risk Crisis

Triple-I “Trends and Insights” Issues Brief: Risk-Based Pricing of Insurance

Stemming a Rising Tide: How Insurers Can Close the Flood Protection Gap