{kind=link}

[ad_1]

Insurance is a data-driven business and underwriting is its coronary heart.

It’s an uncomfortable truth, then, that knowledge from the one longitudinal examine of North American P&C underwriters reveals that many essential elements of underwriting appear to be mired in decline. It is not any overstatement to explain the outcomes of the newest Accenture and The Institute’s underwriting survey as alarming. Underwriting could also be in disaster.

In my earlier put up, we appeared on the survey outcomes from a excessive stage. Today we’re going to zoom in on the findings about underwriting high quality particularly.

Underwriters appear to be shedding religion of their craft

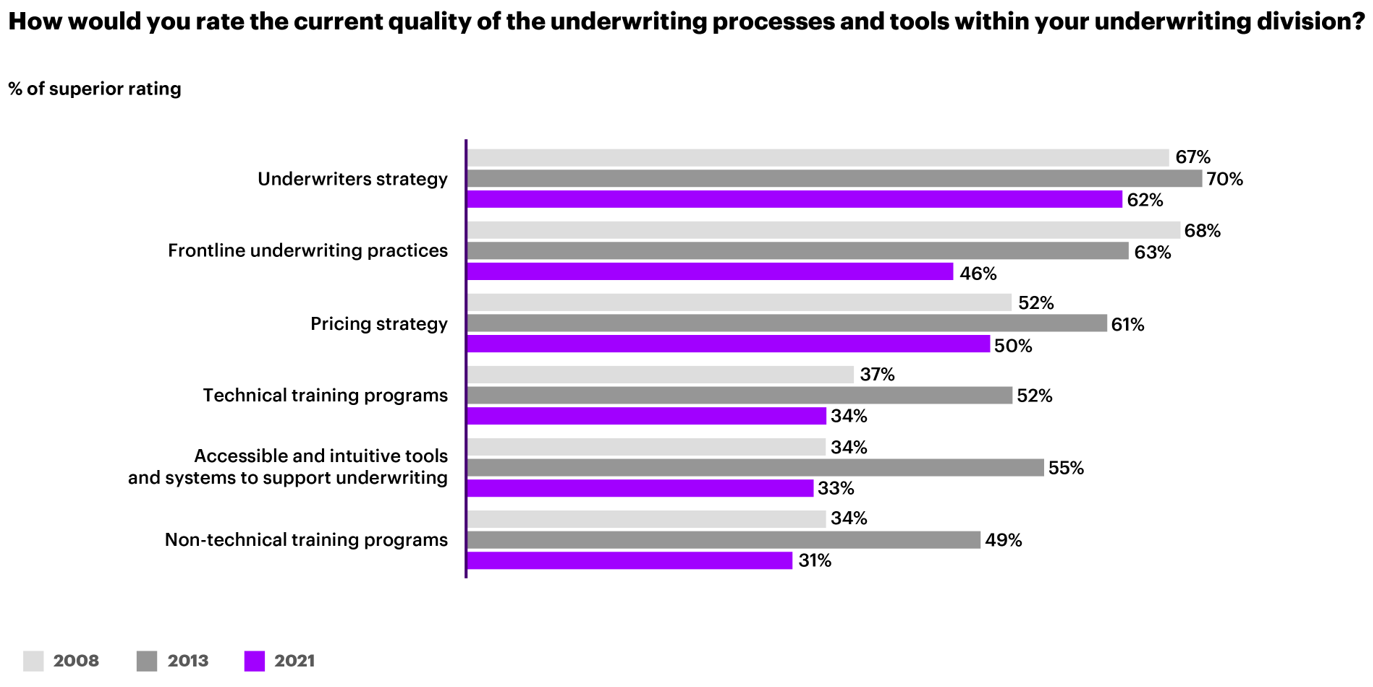

In 2008, 2013, and most not too long ago 2021, we requested underwriters to fee the standard of the processes and instruments they use to do their jobs. The scores for 2021 had been the bottom we’ve seen—although, apparently, the decline has not been uniform.

For instance, 62% of underwriters in 2021 informed us they’d fee their group’s underwriting technique as superior—down 8 share factors from 2013. Likewise, confidence that their group employed a superior pricing technique fell 11 factors, from 61% in 2013 to 50% in 2021.

These are substantial declines, however they’re removed from the most important ones in our most up-to-date knowledge. That doubtful honor goes to confidence within the accessibility and ease of use of the instruments used to help underwriting, which shrank from 55% in 2013 to 33% in 2021. Perhaps extra regarding, confidence in each technical and non-technical coaching, each declined alongside comparable traces.

We additionally requested underwriters to fee the significance of various areas of potential enchancment for underwriting. The prime 4 points recognized had been, so as of the portion of underwriters highlighting them as essential:

-

- Improving the standard and accuracy of knowledge round underwriting submissions (95%)

- Improving coaching and expertise improvement (91%)

- Improving instruments for score and pricing dangers (90%)

- Eliminating non-core duties to permit extra time for danger evaluation (88%)

Change is required—however the place?

My view is that these findings are a transparent indication that many underwriting leaders, amid the business’s rising give attention to bills, progress and analytics, have taken their eye off the ball of conventional underwriting high quality.

This has created an amazing problem for the business, made extra pressing as many markets are softening and the dangers insurers cowl develop extra sophisticated. Do immediately’s underwriters have the abilities they should drive worthwhile enterprise?

It’s in no way clear that they do—however neither is it foregone that they don’t.

In current years underwriters have been outfitted with many highly effective new instruments to assist them measure danger and write insurance policies extra rapidly. Our survey means that these instruments haven’t had the hoped-for influence (and in some circumstances have really made underwriting much less environment friendly).

But the ability of digital instruments to take underwriting to new heights remains to be simple. To reverse the decline instructed by our survey, underwriters and carriers want to shut the hole between the potential of those new instruments and their precise influence on underwriting. This would require altering the service’s inner construction to let underwriters give attention to underwriting.

It can even require making these fashionable underwriting instruments actually accessible and intuitive. instance of that is how underwriting tips are dealt with within the business immediately. In basic, these tips are extra involved with containing each piece of data that might presumably be helpful than they’re with serving to underwriters rapidly, precisely write the chance.

Guidelines as an alternative must be damaged up into items and made match for function in order that underwriters can rapidly and simply discover the data they want when writing insurance policies. Ideally, a tenet system ought to “push” data to underwriters in the intervening time of want as an alternative of requiring the underwriter to “pull” it from a prolonged doc or database.

The digital instruments to make all this occur, after all, are extensively accessible within the business immediately. This survey means that carriers that seize the initiative and implement modifications alongside these traces will see a big bump in underwriting efficiency.

In my subsequent put up, we’ll have a look at what the survey revealed about tech funding in underwriting.

Get the newest insurance coverage business insights, information, and analysis delivered straight to your inbox.

Disclaimer: This content material is offered for basic data functions and isn’t meant for use instead of session with our skilled advisors.

[ad_2]