{kind=link}

[ad_1]

This kind of protection permits aspiring owners to get authorized for a mortgage with as little as 3% down cost. The insurance coverage helps you safe the mortgage with the backing of the insurance coverage company defending the lender.

In this text, Insurance Business discusses how mortgage insurance coverage works in numerous mortgage sorts, how premiums are calculated, and whether or not house consumers can keep away from paying for this extra expense. This can even function a helpful information for these wanting to begin their homeownership journey, so we encourage insurance coverage brokers and brokers studying this to share it with shoppers contemplating beginning this journey.

While mortgage insurance coverage allows house consumers who shouldn’t have adequate funding for a conventional down cost to get mortgage approval, it doesn’t cowl them in the event that they fail to satisfy month-to-month repayments.

Mortgage insurance coverage is designed solely to guard the lender if the borrower defaults on their house mortgage.

By lowering a lender’s threat, this type of protection additionally permits them to lend bigger quantities and approve extra house mortgage functions.

In order for owners to get safety ought to circumstances render them unable to pay out the rest of their house loans, they should buy one other kind of coverage known as mortgage safety insurance coverage (MPI).

Lenders sometimes organize mortgage insurance coverage on the debtors’ behalf. And though such insurance policies cowl the lenders, it’s the debtors who shoulder the price of premiums. There are usually two sorts of mortgage insurance coverage. These are:

- Private mortgage insurance coverage (PMI) for typical mortgage

- Mortgage insurance coverage premium (MIP) for federally backed house loans

Mortgage insurance coverage works barely in another way relying on the kind of mortgage. Here’s an summary of every.

Private mortgage insurance coverage

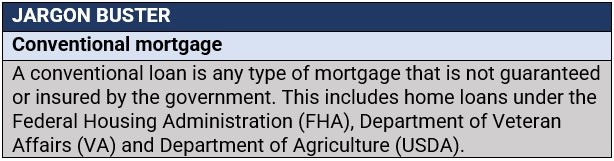

Lenders impose PMI as a requirement for typical loans the place a borrower places out a down cost of lower than 20% of the house’s buy value. This kind of mortgage insurance coverage may additionally be required if a borrower decides to refinance their mortgage and the fairness constructed up is lower than 20% of the property’s worth.

PMI is available in 4 sorts based mostly on how premiums are paid:

- Borrower-paid month-to-month: The most typical kind of PMI whereby the borrower pays month-to-month premiums as a part of their mortgage

- Borrower-paid single premium: Borrowers make one upfront cost or roll the premiums into the mortgage

- Split premium: Borrowers pay a portion of premiums upfront and the rest month-to-month

- Lender paid: Lenders initially shoulder the price of the premium, which debtors pay by means of greater curiosity or mortgage origination charges

Mortgage insurance coverage premium

The premium construction for FHA-backed loans works equally to that of cut up premium PMIs. Apart from a month-to-month MIP that debtors are required to pay no matter their down cost quantity, they should shell out an upfront mortgage insurance coverage premium equal to 1.75% of the bottom mortgage quantity.

VA house loans – designed for navy veterans and their spouses – and USDA-backed mortgages – for consumers of rural houses – don’t require mortgage insurance coverage. Instead, debtors of VA-backed loans pay a funding price between 1.4% and three.6% of the overall mortgage, whereas DA mortgage holders pay an upfront price equal to 1% of the mortgage quantity and an annual price of 0.35% of the overall mortgage.

There are a number of components that dictate the price of mortgage insurance coverage. For PMI, debtors are anticipated to pay between 0.1% and a pair of% of their whole house loans yearly, relying on the next:

- The PMI kind

- Whether the rate of interest is mounted or adjustable

- The mortgage time period or size of the house mortgage

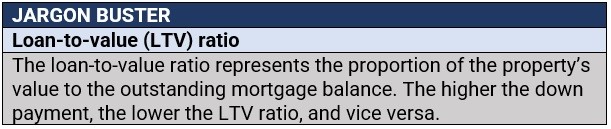

- The loan-to-value (LTV) ratio

- The insurance coverage protection quantity required by the lender

- The borrower’s credit score rating

- The property’s worth

- Whether the premiums are refundable

- Additional threat components decided by the lender

Lenders calculate the PMI premium price, which is usually between 0.5% and 1% of the acquisition value, based mostly on these components to find out a borrower’s threat degree. Premiums are recalculated yearly because the principal is paid off. This implies that the quantity the home-owner must pay in mortgage insurance coverage can also be diminished.

Lenders calculate the PMI premium price, which is usually between 0.5% and 1% of the acquisition value, based mostly on these components to find out a borrower’s threat degree. Premiums are recalculated yearly because the principal is paid off. This implies that the quantity the home-owner must pay in mortgage insurance coverage can also be diminished.

For instance, a purchaser who pays a 5% down cost for a $300,000 house will depart with a traditional mortgage totalling $285,000. If they’re charged 1% PMI, they might want to pay $2,850 yearly or $237.50 month-to-month, which could be included into their common repayments.

Lender-paid mortgage insurance coverage, in the meantime, provides 0.25% to 0.5% to the rate of interest. For FHA-backed house loans, yearly MIP funds sometimes vary between 0.45% and 1.05% of the bottom mortgage quantity.

Most PMI plans enable debtors to cancel their insurance policies as soon as they’ve paid greater than 20% of their whole mortgage quantity, so they don’t have to proceed paying for protection for your entire mortgage time period. Here are another cases the place debtors can cease paying PMI:

- The property’s worth rises build up 25% fairness and the borrower has paid PMI for no less than two years

- The property’s worth rises build up 20% fairness and the borrower has paid premiums for 5 years

- The borrower has put additional funds towards the mortgage principal to succeed in 20% fairness sooner than it could have by means of common month-to-month repayments

Once any of the above situations occur, the borrower must file a proper request to waive PMI, to allow them to keep away from paying pointless premiums. Lenders are additionally mandated by the legislation to routinely cancel mortgage insurance coverage as soon as fairness reaches 22% so long as the borrower recurrently meets month-to-month repayments.

Experts additionally advise debtors to take a proactive strategy and discover out beforehand when they are going to attain the 20% benchmark, so they are going to know when their mortgage insurance coverage funds will finish.

MIPs, in the meantime, are eliminated after 11 years for individuals who have put down no less than a ten% down cost. For debtors with lower than a ten% deposit, they’re required to pay mortgage insurance coverage for the complete size of their house mortgage time period.

Not anymore. Previously, owners had been allowed to deduct mortgage insurance coverage funds from their taxes. This association, nevertheless, has expired after the 2021 tax yr.

The most easy solution to keep away from paying for mortgage insurance coverage is to place out no less than a 20% down cost. This, nevertheless, doesn’t apply to federally backed loans. For house consumers getting an FHA mortgage, there isn’t any method round it. They are required to pay mortgage insurance coverage premiums, no matter how a lot deposit they can put down.

For typical loans, if saving for a adequate down cost will not be an choice, there are nonetheless a number of methods for debtors to dodge this extra expense. These embrace:

First-time house purchaser packages

Most states supply help packages in partnership with native lenders that enable first-time house consumers to take out low down cost mortgages with diminished or zero mortgage insurance coverage necessities. Aspiring owners can contact their state’s housing authorities for extra particulars about these packages.

Piggyback or 80-10-10 loans

In this association, the borrower takes out two mortgages. The first covers 80% of the house’s buy value whereas the second covers one other 10% to 17%. They will then have to put out 3% to 10% down cost, thus the title 80-10-10. The second mortgage, nevertheless, usually comes with a better rate of interest.

Piggyback loans are sometimes marketed as a less expensive choice, nevertheless it doesn’t essentially imply that they’re. Experts nonetheless advocate that debtors evaluate the overall price of one of these mortgage earlier than making a closing choice.

VA-backed loans

Military service members and members of the National Guard or reserves and their surviving spouses could qualify for a VA mortgage. This kind of house mortgage permits a down cost as little as 0% and but doesn’t cost mortgage insurance coverage.

While mortgage insurance coverage can pave the best way to sooner homeownership, consumers additionally have to keep in mind that it’s a further month-to-month price that they should allocate for.

This kind of insurance coverage could also be value paying for individuals who need to climb the homeownership ladder as quickly as attainable however shouldn’t have the time and assets to save lots of for a 20% down cost. This is very true in a property market the place costs are rising sooner than it permits aspiring owners to save lots of or if there’s a restricted time for them to snap up their dream house at a great value.

For a assessment of it from the non-consumer finish, learn this text on important insurances for mortgages to be taught extra about how this operates.

How about you? Do you may have any expertise in taking out mortgage insurance coverage that you simply need to share? Chat us up within the feedback field under.

[ad_2]