{kind=link}

[ad_1]

In this text, Insurance Business examines how this important monetary instrument works within the completely different areas that we cowl, what kinds of advantages it brings, who wants protection essentially the most, and when the very best time is to buy one. If you’re an business skilled trying to find methods to assist life insurance coverage shoppers discover the very best insurance policies, this text can function a helpful information. Just click on the share icon on the highest left of the display.

Life insurance coverage is a kind of insurance coverage coverage that gives a tax-free lump-sum cost to the beneficiaries as soon as the policyholder dies or after a set interval. Because of the monetary profit it affords, life insurance coverage has develop into one in all the preferred types of protection amongst shoppers.

Policies stay in-force so long as the policyholder continues to fulfill premium funds. Some kinds of plans finish after a set time period whereas others present lifetime protection and accumulate money worth.

Life insurance coverage works virtually precisely the identical in several areas, though the coverage names could range. Coverage is available in completely different kinds, with every providing completely different ranges of monetary safety.

United States & Canada

These North American neighbors function the identical programs in the case of life insurance coverage, with protection typically falling into two classes.

1. Term life insurance coverage

As the identify suggests, this sort of coverage covers the policyholder for a set time period. It pays out a demise profit if the insured dies inside a specified interval, which means they will solely entry the cost within the years when the plan is lively. The commonest phrases final for 10, 20, or 30 years.

Term life insurance coverage insurance policies are available in a number of variations. These embrace:

- Decreasing time period life insurance coverage: A renewable coverage with protection reducing over the coverage’s time period at an agreed upon charge.

- Convertible time period life insurance coverage: Can be transformed into everlasting life insurance coverage.

- Renewable time period life insurance coverage: Premiums improve yearly that the coverage is in-force, with charges sometimes the most cost effective within the yr it was bought.

2. Permanent life insurance coverage

Unlike time period life insurance coverage, a everlasting coverage doesn’t expire. Coverage is available in two predominant sorts, every combining the demise profit with a financial savings element.

- Whole life insurance coverage: Offers protection for your complete lifetime of the insured and the financial savings can develop at a assured charge.

- Universal life insurance coverage: Uses completely different premium constructions, with earnings based mostly on how the market performs.

You can learn the profiles of the biggest life insurance coverage firms within the US and the highest life insurers in Canada in our up to date rankings.

United Kingdom

Life insurance coverage insurance policies within the UK additionally are available in two main classes, which work the identical means as these within the US and Canada. These are:

1. Term life insurance coverage

This sort of coverage additionally runs for a hard and fast time period however solely pays out a demise profit if the policyholder dies inside this era. Otherwise, the insurance coverage firm retains all of the premiums paid. There are three sorts of time period life insurance coverage insurance policies:

- Level time period life insurance coverage: Pays out a lump sum if the policyholder dies inside the agreed time period, with the extent of canopy remaining the identical all through.

- Decreasing time period life insurance coverage: The demise profit quantity reduces annually. Such insurance policies are designed for use with reimbursement mortgages, the place the mortgage steadiness likewise decreases over time.

- Increasing time period life insurance coverage: The demise profit quantity rises all through the coverage’s time period to maintain up with inflation.

2. Whole-of-life insurance coverage

Similar to everlasting life insurance coverage in Canada and the US, this sort of coverage offers lifetime protection, with payouts given to the beneficiaries after the policyholder’s demise. Because of the extent of protection, whole-of-life insurance policies have dearer premiums than time period insurance coverage. it has been famous with this sort of coverage that if the policyholder lives longer than anticipated, they will truly find yourself paying greater than they’ll get out of the coverage.

UK residents also can entry over-50s plans, which offer protection for people aged between 50 and 85, with out requiring them to submit medical info. Premiums are sometimes based mostly on the plan holder’s age and the quantity of canopy. Rates, nonetheless, are usually increased as there is no such thing as a means for insurers to foretell the planholders’ danger degree.

The sum assured can also be often capped at round £20,000, whereas ready intervals can final between 12 and 24 months. Additionally, the beneficiaries won’t obtain a profit if the policyholder dies as a result of pure causes throughout this era, however the premiums they paid will likely be returned.

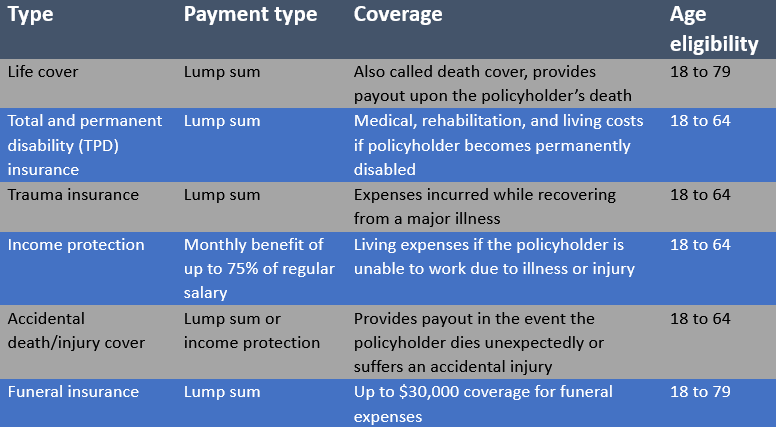

Australia

Apart from offering a demise profit, life insurance coverage insurance policies in Australia supply monetary safety ought to the policyholder develop into critically ailing or disabled. Policies are grouped into six predominant classes, with the extent of protection summed up within the desk beneath.

Each life insurance coverage plan additionally comes with built-in options and advantages, which range from insurer to insurer. The key to discovering the appropriate coverage is to evaluation the product disclosure assertion (PDS). Here are some advantages Australians could need to hold an eye fixed out for when shopping for life insurance coverage:

- Terminal sickness profit: Pays out 100% of the demise cowl prematurely if the policyholder is recognized with a terminal sickness or given lower than 12 to 24 months to dwell.

- Funeral development profit: Benefit ranges from $10,000 to 10% of the sum insured however the policyholder’s household should present a legitimate demise certificates and full declare kinds to obtain the payout.

- Financial recommendation profit: Reimburses the price of monetary advisory companies as much as a selected restrict, often starting from $2,000 to $5,000.

- Future insurability profit: Allows the policyholder to extend their degree of canopy with out the necessity to present extra medical info.

- Premium freeze choice: Lets the policyholder freeze their premiums, so as a substitute of their stepped premiums growing annually, their profit quantity decreases as a substitute.

- Indexation: The degree of canopy rises by a set share between 3% and 5% or the patron worth index (CPI), relying on which is bigger, to maintain up with inflation.

- Interim cowl: Provides a lump-sum cost ought to the policyholder die due to an accident throughout their coverage evaluation. The profit is often the lesser of $1 million or the sum insured on the time of utility.

Here’s what the main life insurance coverage suppliers in Australia supply by way of protection.

An individual’s age and well being standing are the 2 largest components impacting each their eligibility for and the premium costs of life insurance coverage. Because of this, some business specialists say that the very best time to take out this type of protection is whereas an individual is younger and wholesome. They add that as folks become old, well being points additionally start to develop, which might disqualify them from protection and make premiums dearer. Others in contrast the “economic impact” of lacking out on shopping for life insurance coverage whereas youthful to delaying saving for retirement.

https://www.youtube.com/watch?v=YOojvPjc4i0

There are these, nonetheless, who argue that youthful folks are usually confronted with extra bills, together with mortgage, automobile loans, pupil debt, and childcare prices that may profit them to place off shopping for protection. They can also be unsure of the time period length they want as renewing a coverage 10 or 20 years down the street is assured to be dearer.

The backside line is, similar to in different kinds of insurance policies, there is no such thing as a one-size-fits-all life insurance coverage that may cater to each want – and the reply to the query of when the very best time is to take out protection all boils right down to an individual’s distinctive scenario and preferences.

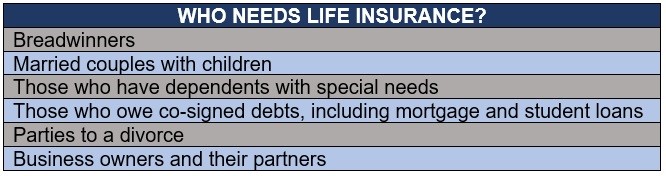

While life insurance coverage can play an important function in offering some degree of monetary safety to a household after a tragic loss, not everybody has a necessity for this sort of protection. Those who’ve constructed up sufficient wealth and belongings to care for his or her household’s wants after they die can forego buying life insurance coverage. However, there are additionally sure teams of people that specialists say will profit tremendously by taking out this type of monetary safety. These embrace:

Different life insurance coverage insurance policies supply completely different advantages. Permanent plans within the US, for instance, can be utilized as a monetary instrument that allows the policyholder to build up wealth. Life insurance coverage, nonetheless, additionally offers a number of sensible advantages. These embrace paying for:

- Funeral, and cremation or burial prices

- Medical payments not lined by medical health insurance

- Estate settlement prices

- Outstanding money owed, together with mortgage, and pupil and automobile loans

- Replacement earnings

- Federal or state taxes

- Inheritance

- Charitable donations

A life insurance coverage coverage covers virtually all kinds of demise, together with these as a result of pure and unintended causes, suicide, and murder. Most insurance policies, nonetheless, embrace a suicide clause, which voids the protection if the policyholder commits suicide inside a selected interval, often two years after the beginning of the coverage date.

Some life insurance coverage suppliers can also deny a declare if the policyholder dies whereas partaking in a high-risk exercise equivalent to skydiving, paragliding, off-roading, and scuba diving.

In addition, an insurer could reject a declare based mostly on the circumstances surrounding the demise. For occasion, if the beneficiary is answerable for or concerned within the policyholder’s demise.

Are you seeking the appropriate life insurance coverage coverage? Which options and advantages do you suppose are important? Should you’re taking out life insurance coverage whilst you’re younger or do you have to wait till you’re a bit older? Use the feedback part beneath to share your ideas.

[ad_2]