{kind=link}

[ad_1]

In this text, Insurance Business delves deeper into this type of protection. We will focus on how any such coverage works, its advantages and disadvantages, and the way it compares to different kinds of life insurance coverage. This is a part of our shopper training sequence. We encourage our regular readers of insurance coverage professionals to move this alongside to shoppers.

Whole life insurance coverage combines lifetime protection with a money worth element that the life insured can entry whereas they’re nonetheless alive. Almost all sorts of everlasting life insurance policies function this fashion. What separates entire life insurance coverage from different sorts of life insurance coverage is that it offers a assured minimal charge of return on the money worth.

According to the Insurance Information Institute (Triple-I), entire life insurance coverage is the preferred type of everlasting life protection. Life insurance coverage can be one of many hottest sorts of insurance coverage that individuals take out.

Whole life insurance coverage gives protection for all the lifetime of the insured – so long as common premium funds are met – and pays out a assured quantity on the time of their dying. There are two principal sorts of entire life plans:

- Non-participating entire life insurance coverage: Provides a tax-free dying profit with lifetime protection and accumulates a assured money worth that policyholders can borrow in opposition to.

- Participating entire life insurance coverage: In addition to the assured dying profit, this may generate dividends, relying on how the insurer performs, that are usually issued to the policyholder yearly.

Most entire life insurance coverage insurance policies function with degree premiums, that means the charges stay the identical throughout the coverage. Some plans comply with a restricted cost construction the place the insured pays larger premiums within the first few years of the coverage earlier than the charges go decrease within the latter years. Others undertake a modified premium mannequin, which works the other, imposing decrease premiums early within the coverage earlier than charges improve.

A portion of those premiums goes to the coverage’s financial savings element, permitting it to build up money worth on a tax-deferred foundation over time. The insured can entry this quantity in 3 ways:

- Applying for a mortgage: A tax-free choice, policyholders pays the quantity again, with a corresponding curiosity.

- Withdrawal from the coverage: If the quantity withdrawn is lower than the portion of the money worth attributable to the premiums paid, no taxes apply. If the quantity is bigger, taxes are imposed as a result of the distinction is taken into account funding features.

- Surrendering the coverage: By doing so, the insured will obtain the money worth minus the give up cost. They may also must pay revenue taxes on any funding features that have been a part of the money worth.

One factor to notice is that by surrendering the coverage, it successfully terminates the plan, so this could solely be completed if the policyholder not wants protection or if they’ve a brand new life insurance coverage plan in place.

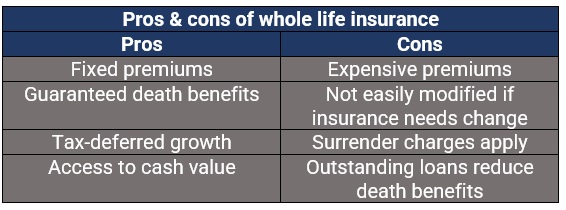

One of the principle benefits of taking out an entire life insurance coverage plan is that it may be used as a financial software to build up wealth. Here are among the advantages of any such everlasting life coverage:

- Lifetime protection: Policies cowl the insured for all times, in contrast to time period life insurance coverage, which ends protection after a set variety of years.

- Tax-deferred development: Whole life insurance coverage permits the policyholder to speculate on a tax-deferred foundation, that means they’re exempt from paying taxes on any curiosity, dividends, or capital features on the plan’s money worth, until they withdraw the proceeds.

- Access to money worth: Policyholders can borrow in opposition to the money worth of a complete life insurance coverage coverage if the necessity arises with out incurring penalties, in contrast to in tax-advantaged retirement plans akin to 401(ok).

- Accelerated advantages: Insureds could possibly obtain between 25% and 100% of their coverage’s dying profit even when they’re nonetheless alive if they develop a important sickness – together with invasive most cancers, coronary heart assault, renal failure, or stroke – and use the cash to pay for medical payments.

The principal downside of entire life insurance coverage is the worth. Premiums are usually dearer in comparison with these of different sorts of life insurance coverage insurance policies. Compared to these for time period life plans, as an illustration, the charges for entire life insurance policies might be as much as 15 instances dearer for a similar dying profit.

Another drawback is that policyholders can’t simply finish the coverage. If they notice that they not want the protection or can’t afford the month-to-month funds, insurers could impose a give up cost ought to they resolve to stroll away from the plan. The quantity is often 10% of the money worth, relying on how far alongside they’re with the coverage, however decreases because the years go by.

In addition, if the insured decides to faucet into the coverage’s money worth and fails to pay again the mortgage, this may scale back the dying profit quantity.

Here’s a abstract of the professionals and cons of a complete life insurance coverage coverage.

A complete life plan’s money worth operates the identical manner as a retirement financial savings account. Both enable the worth to construct up on a tax-deferred foundation.

As the portion of the premiums that go in direction of the coverage’s money worth grows, the insureds can borrow in opposition to or withdraw from the amassed quantity. Typically, the money worth builds up quicker the youthful the policyholder is and slows down as they get older because of the elevated dangers related to age.

Policyholders can faucet into the money worth and use it for no matter they deem obligatory, together with as month-to-month premium funds to their entire life insurance coverage. One factor to notice is that any excellent loans and withdrawals can scale back the quantity their beneficiaries are set to obtain.

However, most entire life insurance coverage solely pay out the dying profit, no matter how a lot money worth the coverage has amassed over time. Often used as a manner for insurers to reduce threat, this quantity reverts to them on the time of the insured’s dying – until the policyholder purchases a particular sort of rider that offers the beneficiaries possession of the amassed money worth. More on this later.

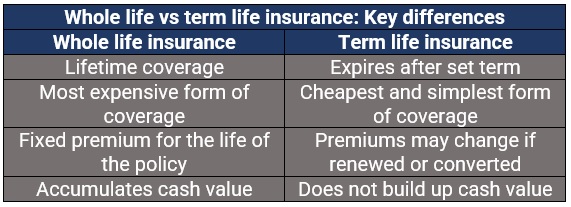

Despite being in the identical insurance coverage class, time period life and entire life insurance policies have a number of key variations. Here are a few of them:

Coverage interval

Unlike entire life insurance policies, which offer lifetime protection, time period life insurance coverage covers the policyholder for a set time period, often 10, 15, 20, and 30 years – the longest plan that one can take out. It pays out the profit if the insured dies inside the specified interval, that means they will solely entry the cost within the years that the coverage is lively.

Premium costs

Premiums for time period life plans additionally are usually decrease as it’s extra seemingly that the policyholder will outlive the coverage. Term life insurance coverage, nonetheless, might be renewed or transformed right into a everlasting life plan.

Cash worth

Term life insurance policies don’t accumulate money worth, in contrast to entire life insurance coverage. This means the insured can’t borrow in opposition to their insurance policies or get any money worth again in the event that they cancel.

The desk under summarizes the important thing variations between entire life and time period life protection.

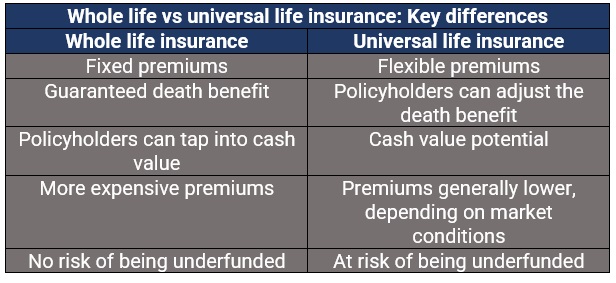

Permanent life insurance coverage are available in two principal varieties – entire life insurance coverage and common life insurance coverage. While each sorts of insurance policies have key similarities – like offering lifetime protection and mixing the dying profit with a financial savings element – there are additionally main variations. These embrace:

Flexible premiums

Unlike entire life plans the place premiums keep the identical throughout the coverage, common life insurance coverage makes use of a versatile premium construction, which the policyholder can regulate relying on their protection wants. This, nonetheless, is topic to sure limits. That is why any such protection can be referred to as adjustable life insurance coverage.

Cash worth assure

While the money worth in entire life plans present assured returns, the returns for common life insurance coverage are primarily based on how the market performs. The principal downside of that is that it may end up in the plan turning into underfunded. This, in flip, could cause premiums to rise considerably and if not paid, can result in the termination of the coverage.

The desk under sums up the important thing variations between entire life and common life insurance coverage.

Compared to these for a time period life coverage, entire life insurance coverage premiums might be considerably dearer. An evaluation completed by the comparability web site Finder of annual insurance coverage charges reveals a distinction of 1000’s of {dollars} between a time period life and an entire life plan.

Just like different sorts of life insurance coverage, premiums for entire life insurance policies are impacted by a variety of things, together with:

- Age

- Gender

- Height and weight

- Past and present well being situations

- Family’s medical historical past

- Eating habits

- Smoking standing, together with marijuana

- Substance abuse

- Credit score

- Criminal historical past

- Driving document

- Hobbies and actions

Additionally, the price of an entire life insurance coverage coverage might be influenced by the next:

- Payment interval: Policyholders could choose to pay all the coverage in a sure interval, 10 or 20 years as an illustration, pushing up premiums considerably.

- Guaranteed return charge: Some insurers supply the next assured return, which may additionally improve charges.

- Dividend crediting: Receiving your dividend funds as a credit score towards premiums can decrease the quantity policyholders need to pay yearly.

Life insurance coverage corporations supply a variety of add-ons that policyholders should buy to entry additional protection and assist them take advantage of out of their insurance coverage insurance policies. These riders include corresponding prices. Here are some add-ons out there for entire life insurance coverage policyholders.

- Accelerated dying profit rider: An ordinary inclusion in most insurance policies, this pays out the profit if the life insured will get critically sick or turns into disabled.

- Child life insurance coverage rider: Provides a small profit to cowl funeral or burial bills for kids.

- Early or enhanced money worth rider: Adjusts the give up prices if the policyholder must give up the coverage within the first few years.

- Estate safety rider: Helps offset property taxes that could be due.

- Guaranteed insurability rider: Allows the insured to extend the dying profit with out going via one other full utility course of.

- Long-term care insurance coverage rider: Enables the policyholder to make use of part of the dying advantage of in the event that they require long-term care. This is usually a less expensive choice than taking out a separate long-term care coverage.

- Overloan safety rider: Prevents the coverage from lapsing as a consequence of mortgage balances exceeding the money worth.

- Waiver of premium rider: Allows the policyholders to cease paying premiums in the event that they turn out to be critically sick or disabled.

Whether entire life insurance coverage is value it relies on an individual’s objectives and circumstances. For those that worth predictability, an entire life insurance coverage coverage could also be value contemplating because it gives everlasting protection with premiums that keep the identical no matter an individual’s age or well being standing. It additionally builds money worth over time that policyholders can faucet into to pay for medical payments or different bills.

What about you? Do you assume entire life insurance coverage is value contemplating? Do you’ve got an expertise about everlasting life insurance policies that you simply need to share? Use the feedback part under in your ideas.

[ad_2]