{kind=link}

[ad_1]

An important a part of an insurance coverage contract, a deductible is the quantity the policyholder agrees to pay out of pocket earlier than the insurer shoulders the price of protection.

One essential factor to notice, nonetheless, is that though it’s common within the trade to listen to “after paying for a deductible,” more often than not, policyholders don’t truly pay something to their insurance coverage suppliers. Rather, they pay for one thing equal to the deductible quantity – automobile repairs or medical assessments, for instance – then the insurer pays out for the remainder of the protection as much as the utmost restrict.

In some situations, insurance coverage corporations subtract or deduct – therefore the time period deductible – the quantity from the insured loss earlier than paying out as much as the boundaries of the coverage.

You can try the which means of widespread insurance coverage trade phrases in our jargon buster.

The Insurance Information Institute (Triple-I) describes a deductible as “how risk is shared between the policyholder and the insurer.” This can be the rationale why insurance coverage insurance policies have deductibles.

Because they share the price of the claims with the policyholders, insurance coverage suppliers can keep away from receiving a barrage of small and cheap claims, to allow them to concentrate on main losses, which insurance coverage insurance policies are designed for.

In a method, having deductibles can even make policyholders assume twice about partaking in dangerous behaviors or not performing in good religion as they are going to be financially impacted by any loss or injury as properly. This successfully aligns the curiosity of the insured with that of the insurer, which is to mitigate the chance of main losses.

There are two methods how insurers impose deductibles in an insurance coverage coverage:

- Standard deductible: Indicates a selected greenback quantity to be paid out in an occasion of a declare.

- Percentage deductible: Defines a selected proportion of the coverage restrict to be paid out in an occasion of a declare.

The deductible quantity is indicated within the phrases of protection on the declarations web page, or the primary web page, of an insurance coverage contract.

According to Triple-I, state insurance coverage rules strictly dictate the way in which deductibles are included into the coverage’s language and the way these are carried out, though legal guidelines can fluctuate between states.

Almost all insurance coverage insurance policies include a deductible, apart from life insurance coverage, the place the beneficiaries obtain a tax-free lump-sum cost after the policyholder dies.

A single coverage can also have a number of deductibles as every protection could have its personal deductible quantity. The solely exception is medical insurance, the place plan holders normally want to satisfy a single deductible for a whole calendar 12 months.

Here’s how insurance coverage deductibles work for the various kinds of insurance coverage insurance policies.

In house insurance coverage, deductibles apply solely to property injury. Homeowners don’t have to pay a deductible for legal responsibility claims. The deductible additionally applies every time a declare is filed.

For insurance policies with commonplace or dollar-amount deductible, the deductions work fairly simple – the quantity specified within the contract will likely be subtracted from the claims payout. If a coverage has a $500 deductible, as an example, then the insurer can pay the policyholder $9,500 for an insured loss value $10,000.

For plans with a percentage-based deductible, the quantity the insurance coverage firm covers is calculated based mostly on a proportion of the property’s insured worth indicated within the coverage doc. For houses insured for $250,000 with a 2% deductible, for instance, the insurer will ship the home-owner a claims examine for $24,500. Percentage deductibles usually apply solely to house insurance coverage insurance policies, and to not different sorts of plans.

Disaster deductible: How does it work?

While commonplace owners’ insurance coverage insurance policies cowl wind, hail, storm, and hurricane injury, safety towards sure sorts of calamities – together with flooding and earthquake – should be bought individually.

Many house insurance coverage include particular deductibles – additionally known as catastrophe deductibles – that apply to claims attributable to completely different pure calamities. Here’s how they work:

- Hurricane deductibles: Typically following a percentage-based mannequin, hurricane deductibles are sometimes increased than different sorts of house insurance coverage deductibles. Some US states give owners the choice to take out an ordinary deductible in trade for dearer premiums, so long as the home shouldn’t be positioned in a hurricane-prone space.

- Wind and hail deductibles: Working much like hurricane deductibles, wind and hail deductibles are generally based mostly on a proportion of the house’s insured worth, normally ranging between 1% and 5%.

- Flood insurance coverage deductibles: Available in commonplace or percentages, the deductible quantity varies relying on the place the house is positioned and the insurance coverage supplier. Policyholders can even select completely different deductibles for the home and private belongings.

- Earthquake insurance coverage deductibles: These observe a percentage-based mannequin, starting from 2% to twenty% of the house’s alternative worth. Insurers in earthquake-prone areas usually set the minimal deductible quantity at 10%.

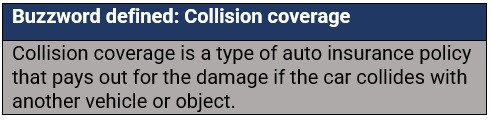

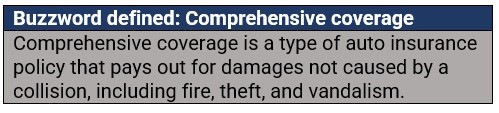

These deductibles work virtually the identical method as these for house insurance coverage, besides that percentage-based deductibles don’t apply. Policyholders additionally pay deductibles just for automobile injury and never for legal responsibility claims.

Generally, automobile insurers permit motorists to decide on separate deductibles for collision and complete protection, even when they’ve the identical quantity.

Disappearing deductible: How does it work?

A disappearing deductible – additionally known as a diminishing or vanishing deductible – is an extra protection in an auto insurance coverage coverage that decreases the deductible quantity annually that the policyholder maintains a clear driving document. It can be a method for automobile insurance coverage corporations to reward secure drivers.

For every accident- and claims-free 12 months, a motorist can earn sure disappearing deductible credit, which may accumulate and be used to scale back the deductible quantity of their collision and complete insurance policies. It can be attainable for drivers to succeed in $0 deductibles in the event that they preserve a clear driving document lengthy sufficient.

The credit sometimes reset as soon as the policyholder makes a declare or is concerned in a automobile accident.

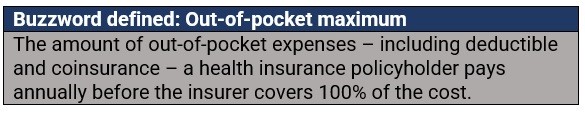

Unlike in house and auto insurance coverage insurance policies the place every protection could have its personal deductible quantity, medical insurance plan holders are required to satisfy a single deductible for a whole 12 months. After they max out on their deductibles, they may then break up the prices with their insurer in a system referred to as coinsurance till they attain their out-of-pocket most.

Coinsurance follows a percentage-based mannequin. For instance, in a 20%-80% break up, the plan holder pays 20% of the healthcare prices whereas the insurer covers the remaining 80% till the out-of-pocket restrict is reached. Once they hit this restrict, the insurance coverage firm then pays 100% of their healthcare bills for the remainder of the 12 months.

Depending on the medical insurance plan, policyholders could have a person or household deductible, or a mixture of the 2. An particular person deductible applies to plans with single protection and works the identical method described above.

Family deductibles, in the meantime, are available two varieties:

- Aggregate deductible: One whole deductible for the entire household.

- Embedded deductible: Apart from a household deductible, there are additionally particular person deductibles for every member of the family.

Premiums and deductibles are two of the main out-of-pocket prices related to insurance coverage, which is why they could typically be confused with each other. While an insurance coverage premium is the quantity a policyholder pays in trade for protection, a deductible is the quantity the insured must pay for damages earlier than protection kicks in.

These two, nonetheless, have an inverse relationship. As one will increase, the opposite decreases, so usually the upper the deductible, the decrease the insurance coverage premium, and vice versa.

Is it higher to have a better or decrease insurance coverage deductible

When it involves insurance coverage insurance policies, is it higher to have a better or decrease deductible?

According to some specialists, selecting a decrease deductible is sensible if the policyholder expects to entry protection extra usually or in the event that they won’t be able to afford massive out-of-pocket bills. These could also be as a result of they’re uncovered to increased ranges of dangers or haven’t saved sufficient for an emergency fund.

Meanwhile, a better deductible could be a good possibility for policyholders who don’t anticipate to make a number of claims. This technique additionally permits them to scale back insurance coverage prices and allocate the additional cash to their financial savings.

What about you? Do you favor a better or decrease insurance coverage deductible? How a lot deductible quantity do you assume is correct for every insurance coverage plan? Share your ideas within the feedback part beneath.

[ad_2]