{kind=link}

[ad_1]

Automotive is now all about mobility. And automotive insurance coverage is within the midst of an enormous change. If you watched the Superbowl this previous Sunday and also you had been like me ready for all of the commercials, you probably noticed two specific advertisements which have a bearing on the way forward for automotive insurance coverage. Netflix’s partnership advert with GM, promising to make use of extra EVs of their reveals, and the announcement of Dodge’s new EV truck — which implies that now all three of the standard U.S. massive three automakers have electrical vehicles.

This highlights the fast progress of EV and Autonomous car use, however the progress of EV and autonomous vehicles will probably be one of many “revolutionary” improvements of our time, even contributing to the continued fast progress of truck gross sales sooner or later. This is only one storyline within the epic sweep of technological change in automotive circles, however this story has a twist that entails residence insurance coverage as properly.

Two conventional considerations for truck patrons are:

- Mileage vary — is the gasoline tank large enough to cut back fill-ups?

- Hauling and towing energy — is there sufficient horsepower and torque to hold heavy hundreds simply?

For an electrical truck to compete with a gasoline truck on each of those factors, the EV batteries have to be very massive and highly effective. In truth, they must be so highly effective that their energy rivals backup battery methods for houses. The Ford Lightning has been in comparison with proudly owning 7 Tesla Powerwalls (a house backup battery system).[i] Knowing this, engineers have created superior electrical panels and methods that may deal with bi-directional charging — charging that may feed energy each into and out of the house. Both Ford and GM vehicles may have the aptitude to do that; powering houses if the ability goes out (for as much as 21 days, in response to GM), identical to a backup battery or generator. GM additionally theorizes that many EV homeowners might be feeding energy again onto the grid.

In truth, GM not too long ago spun off GM Energy, a brand new enterprise unit devoted to “EV related products for residential and commercial customers.”[ii]

However, should you mix the expansion of photo voltaic panels (for charging EVs) and the necessity for superior electrical in current houses, a few of these mobility developments could create new residence property danger. This is only one extra method that the limitations are coming down in insurance coverage traces of enterprise.

Mobility — danger in movement

The automotive world is quickly altering in all dimensions because of the shift in how different firms and industries are altering, equivalent to ridesharing, the usage of different mobility choices equivalent to electrical bikes, autonomous automobiles, altering views of auto possession, developments in automotive know-how, together with a rising plethora of transportation choices like automotive sharing.

Companies outdoors insurance coverage are coalescing round a shift to “mobility.” Mobility choices are vital, however they are often fulfilled by many means past conventional car utilization or possession…a major shift impacting enterprise fashions from automotive firms to dealerships, rental automotive firms, ride-sharing firms, car-sharing firms, insurance coverage firms, and extra. Risk exists in all aspects of mobility. Seattle, for instance, is thought for its excessive pedestrian damage and fatality charges. Urban dwellers are more and more dwelling with out automobiles, but they nonetheless transfer from place to put they usually nonetheless incur danger.

Highly networked, data-driven, mobility enterprise fashions are quickly rising, primarily outdoors of insurance coverage. Automotive firms like Tesla, Ford, and GM are main this shift together with ride-sharing platform firms like Uber. They are redefining the client journey and the whole buyer relationship throughout a broader set of transportation or mobility choices. As a outcome, the risk for auto insurance coverage is for insurers to proceed a 100+-year-old viewpoint — seeing a coverage as a transaction.

In Majesco’s recently-released Consumer Survey Report, Enriching Customer Value, Digital Engagement, Financial Security and Loyalty by Rethinking Insurance, we have a look at buyer developments via the lens of insurer influence. We use these developments to think about how information use and a holistic view of the client may help insurers develop extra related to a altering mobility surroundings.

In right now’s weblog, we’ll have a look at the survey information and take into account 3 ways wherein insurers can meet buyer demand:

- Personalized pricing with information

- Meeting the demand for value-added providers

- Expanding channel choices

Personalized Pricing with Data

In the digital period of insurance coverage, information is the gasoline for optimization and innovation. New applied sciences, demographics, and behaviors are driving the explosion of information and can energy the expansion and management positions for insurers over the following 10 years. At the forefront of that is auto insurance coverage.

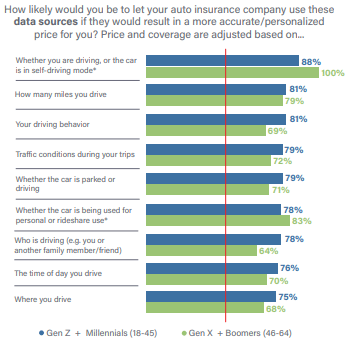

Interestingly, there may be robust alignment between each generational teams in utilizing new, non-traditional sources of information for personalised pricing for auto insurance coverage as represented in Figure 1. Connected units (and different information sources) allow pricing primarily based on mileage, utilization, and driving habits, which might decrease premiums and deal with the monetary top-of-mind difficulty for customers.

Acceptance is on the rise.

Gen Z and Millennials’ curiosity in utilizing each information supply (all sources obtained optimistic approval of 75% or increased) displays the openness of this era to personalize insurance coverage with their information. Gen X and Boomers who’re rideshare drivers or use self-driving capabilities have exceptionally excessive ranges of curiosity in utilizing car information for pricing. With the automotive firms shifting on this path, the strain might be on for insurers to supply related pricing choices.

With the work choices shifting to distant/hybrid and fewer driving in consequence, customers are more and more involved in pricing primarily based on precise car utilization and driving habits, quite than the standard method. The work choice adjustments proceed to dramatically cut back the variety of miles pushed, spurring elevated curiosity in data-driven and behavior-based insurance coverage.

Figure 1: Interest in new information sources for auto insurance coverage pricing

Demand for Value-Added Services

Gen Z and Millennials are strongly involved in value-added providers included with their auto insurance coverage, mirrored within the 80% or increased response on all 10 gadgets, as seen in Figure 2. Gen X and Boomers share their highest ranges of curiosity with Gen Z and Millennials on 5 of these things. Three of those deal with safety-related alerts: detecting a crash and alerting emergency providers; alerts about street circumstances, visitors, and climate; and alerts about car recollects. The different two deal with holding their car in secure working situation and in compliance with license and registration renewals. Increased use of auto security know-how places extra emphasis on prevention and fewer on conventional indemnification.

With all of the adjustments to automobiles and their use, insurers must proactively rethink conventional auto insurance coverage from a definite transaction to part of a broader buyer mobility answer that adapts and adjustments in actual time primarily based on buyer wants and behaviors.

Figure 2: Interest in value-added providers with auto insurance coverage

Expanding Channel Options

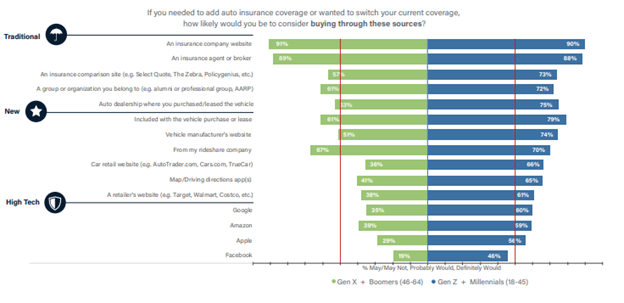

Traditional channels stay dominant in auto insurance coverage buying, with a choice for firm web sites and brokers/brokers reaching the 90% degree for each era segments. (See Figure 3.) All different channels drop underneath 80%, but practically all channels have a excessive degree of curiosity. Vehicle buy/lease is the following highest for Gen Z and Millennials at 79% and 61% for Gen X and Boomers. The robust exhibiting of this channel is one other spotlight of the rising reputation of embedded insurance coverage, which is a superb match for car buying, renting, and leasing.

Once once more utilizing a 50% reference line highlights the dramatic gaps between the era segments throughout the channel choices. Gen Z and Millennials’ curiosity exceeds 50% on 14 of the 15 channel choices (93%), whereas Gen X and Boomers have solely 8 of 15 (53%) exceeding 50%, highlighting the necessity for expanded channel choices to succeed in the youthful era when and the place they need.

The new and high-tech channels all replicate embedded insurance coverage alternatives for the youthful era, a rising space of focus for insurers and automotive firms. The new and rising spectrum of channel choices now accessible, particularly the thrilling alternatives for embedded insurance coverage, will give modern insurers and their companions super alternatives for progress, with new markets, new choices, and glad, loyal clients.

Figure 3: Interest in channel choices for auto insurance coverage

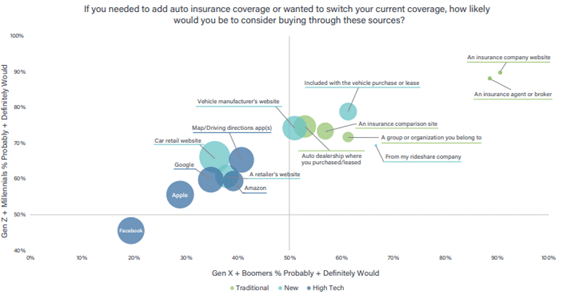

In Figure 4, we will see these developments from the angle of generational alignment. Traditional insurance coverage firm web site and brokers/brokers channels (within the higher right-hand nook) present each their energy of choice and excessive degree of settlement between the generations. The chart additionally highlights the enchantment of 6 different channels for the auto insurance coverage market: rideshare firm, affinity teams, embedded with the car buy/lease, comparability websites, auto dealerships, and car producers’ web sites.

Figure 4: Generational alignment on curiosity in channel choices for auto insurance coverage

Ease of channel use in opposition to GAFA manufacturers

Of course, channel curiosity can be a mirrored image of present perceptions. In each case, the respondent is someway contemplating how simple or precious they understand a channel to be. This is likely one of the causes that we generally ask questions concerning Google, Amazon, Facebook, and Apple. If these widespread buyer manufacturers are perceived as easy for different transactions, will that be accounted for when a buyer considers the place they may buy their auto insurance coverage?

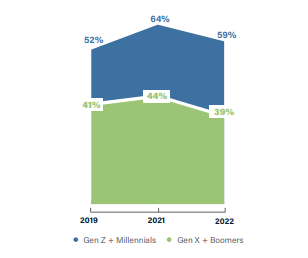

In Figure 5, we see an fascinating development concerning Amazon. It has achieved rising curiosity over the previous a number of years with Gen Z and Millennials as a channel choice for auto insurance coverage. Interest elevated by 12 share factors in 2021 over 2019 however settled barely decrease at 59% on this 12 months’s survey. In distinction, Gen X and Boomer curiosity in Amazon as an auto insurance coverage channel is barely decrease and has remained regular, however nonetheless must be thought of an vital and helpful channel for a large portion of the Gen X and Boomer market.

Figure 5: Trend in curiosity in Amazon as a channel for auto insurance coverage

Holistic approaches to insurance coverage ecosystems

The mixture of know-how and buyer expectations is instantly impacting insurance coverage by altering the standard ecosystem of brokers and brokers, to new channel ecosystem choices equivalent to embedded, automotive, transportation companies, massive tech, and extra. By doing so, it breaks down enterprise and market boundaries to make the ecosystems fluid, primarily based on buyer wants and expectations for each the danger product and different value-added providers that had been recognized on this analysis. This creates larger worth for insurers via new income streams and entry to a broader market via the multiplier impact.

Insurers should take into account these impacts, nonetheless, outdoors of a singular line of enterprise. Majesco’s report not solely hyperlinks all private traces, nevertheless it highlights the concept that insurance coverage is now, greater than ever, a part of a holistic method to monetary wellness that must be checked out as an entire…simply as usually as it’s checked out via a singular line. Our instance of EVs “engaging” with the house in a symbiotic electrical system is a living proof — the boundaries are falling. How is the danger profiles altering with the usage of these new mobility choices? It’s not black and white.

Who we’re as cell folks — switching seamlessly via transportation modes and life/work wants — have to be acknowledged by insurers via personalization, related merchandise, and an entire understanding of how and the place we want to purchase.

For an entire have a look at buyer sentiments and insights concerning insurance coverage wants, merchandise, providers, and channels, remember to learn Majesco’s thought-leadership survey report, Enriching Customer Value, Digital Engagement, Financial Security and Loyalty by Rethinking Insurance.

[i] Csere, Csaba, Can Your EV Power Your House?, Car and Driver, May 11, 2022.

[ii] Newcomb, Doug, GM establishes new unit to assist join EVs with the ability grid, Automotive News, October 11, 2022.

[ad_2]