{kind=link}

[ad_1]

In the realms of trigger and impact, nothing fairly stacks as much as innovation for its means to create optimistic change in any group.

When insurers first heard that AM Best could be assessing innovation, some had been skeptical. Insurers are all completely different. Unique merchandise would name for various ranges of innovation. How might innovation really be measured in a means that is sensible and in addition doesn’t penalize these areas of the trade that don’t want dramatic innovation? Is there something to really be gained within the course of, or is that this simply one other strategy to assess the worth of a corporation? Is there any correlation between innovation and profitability? Is there any relationship between innovation and total enterprise power? Operationally and strategically, the place are insurers on the roads of innovation?

I requested two trade consultants to hitch me in a webinar entitled, Insurance Transformation — Operationally and Strategically — Where are We?

Our aim was to take a look at innovation from a minimum of two angles. First, we needed to take a look at the apply of innovation and the way it may play a job in furthering the targets of the group. Instead of sticking with principle, we requested an AM Best knowledgeable to present us his innovation perspective utilizing actual AM Best findings from insurers who had reported on their innovation standing. Second, we needed to take a look at the technique of innovation. How a lot of a precedence do insurers want to present to innovation in the event that they hope to enhance their long-term profile for progress?

We cut up this interview into two sections. Today’s weblog covers each the present standing and principle of innovation efforts. The second will cowl the apply of innovation from the attitude of various traces of enterprise.

Our three consultants on the September webinar panel had been:

Edin Imsirovic, Associate Director, AM Best

Seth Rachlin, Executive VP, Global Insurance Industry Leader, Capgemini

And myself, Denise Garth, Chief Strategy Officer, Majesco

To kick us off, I requested Edin Imsirovic to stroll us via the AM Best Innovation evaluation. He answered lots of our questions beneath.

What is the Innovation Score and the way did it come to be part of the “official criteria” of an AM Best score?

Edin Imsirovic

Discussing company-specific innovation is absolutely nothing new. We have at all times talked about corporations’ progressive methods and have analyzed their deal with innovation. It’s at all times been part of our score course of. So why did AM Best attempt to individually assess innovation with a separate evaluation?

The largest purpose is the accelerated nature of change. During occasions of speedy change, being progressive is very necessary as a result of enterprise fashions might evolve or change extra quickly. Before we launched the innovation standards, we did an trade survey and located that just one% of the trade doesn’t see innovation as crucial. So, given the trade’s view of the significance of innovation in occasions of accelerated change, we determined to be proactive in addressing these traits by highlighting this specific facet of insurance coverage and making the evaluation of innovation extra express. It took us about two years of working with the trade and varied tutorial establishments to develop the innovation rating.

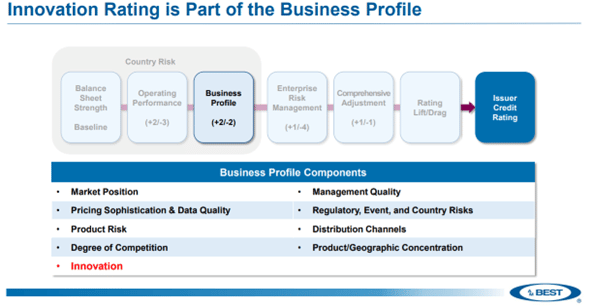

How does the Innovation Assessment function throughout the Business Profile?

Edin Imsirovic

AM Best nonetheless has the identical constructing block method to the score course of. We begin our evaluation with coverage power, after which we take a look at forward-looking elements like working efficiency, enterprise profile, and enterprise threat administration. Historically, the enterprise profile has completely different elements; issues like market place, administration, high quality, and so forth. (See Fig.1)

Figure 1: Innovation Rating

Innovation is now the ninth part. Our perception is that innovation or lack of innovation can both improve or erode the monetary power of the insurer.

We take an enter and output method to measuring innovation, each of that are weighted equally. For enter, we charge management, tradition, and sources which are devoted to innovation, in addition to processes and constructions associated to innovation. When we take a look at the output, we take a look at the extent of transformation associated to innovation, tied to quantifiable outcomes.

Has AM Best seen a correlation between innovation scores and AM Best scores?

Edin Imsirovic

Yes. It turned obvious that probably the most progressive gamers like these within the chief or outstanding classes had been capable of differentiate themselves by credibly quantifying the outcomes proper on the output of their innovation efforts. The leaders distinguish themselves by being the progressive first movers throughout the insurance coverage house. They had been sometimes the timeliest in responding to market pressures by providing new merchandise or options for rising wants. Leaders sometimes had very excessive transformational scores.

As you’d anticipate, the upper rated the corporate is, the upper the innovation scores.

Which traces of enterprise appear to be probably the most progressive?

Edin Imsirovic

Every line of enterprise has progressive gamers, however as we had been conducting innovation assessments all through our universe, we seen sure themes associated to innovation. For instance, these with both the best competitors or these with probably the most structural or technological change additionally tended to be the extra progressive gamers. The most progressive traces of enterprise we recognized had been reinsurance, well being, and private auto traces.

Personal traces, generally, are particularly uncovered to altering client tastes and preferences and better client expectations. Consumers are drawn towards seamless and personalised person experiences. Insurers are more and more dealing with expectations which are set by different industries moderately than by direct rivals.

We are also seeing more and more how insurance coverage corporations are turning to innovation to handle high quality, which is a outstanding concern of medical health insurance. Health insurance coverage is anxious with each the standard of customer support and the supply of high quality well being care.

Let’s take a look at a high-level abstract concerning enterprise outcomes. Is there any correlation between innovation scores and progress charges?

Edin Imsirovic

You can see a really fascinating and clear delineation between innovation classes associated to premium progress. Innovators grew their premium over a five-year interval at roughly 12%. Moderates grew at 9%. Companies with minimal innovation grew at 8%.

We additionally seen that innovation and provide and progress are linked. Digital developments have enabled extra progressive insurance coverage to realize market share. The divergence in premium progress was significantly acute throughout COVID.

Insurers that already had digital infrastructures had been usually capable of proceed roughly regular operations. For instance, the common internet premium charge and progress in 2020, which was the height COVID 12 months, was about 7% for innovators. Premium progress for reasonable innovation was about 4%. Those with minimal innovation assessments had been beneath 2%.

Those categorized as leaders in innovation additionally tended to have decrease expense ratios. They have made optimizing working effectivity via innovation an important a part of their technique.

The Economy’s affect on innovation. Should the trade pull again or transfer ahead? What ought to enterprise priorities be, in gentle of right this moment’s macroeconomic elements?

Denise Garth

We have various macroeconomic challenges that every one companies, together with insurance coverage, are starting to face. They will have an effect and an affect on innovation plans and budgets and priorities shifting into 2023 and past. I might categorize them into eight areas.

- Optimize & Innovate Business — proceed to optimize whereas creating innovation round both the prevailing or future enterprise.

- Risk Resilience — deal with threat prevention and threat mitigation to keep away from claims and enhance buyer expertise.

- Customer Expectations — take a look at the expectations which are driving the enterprise.

- Personalized Niche Products — match smarter buyer spending by insuring and underwriting based mostly on way of life/conduct/enterprise want.

- Market Reach & Growth — permit clients to purchase insurance coverage otherwise, via further channels and embedded choices.

- Ecosystem and APIs — foster partnerships and distribution preparations that rely on APIs which permit insurers to attach.

- Long-term Data Strategy — increase knowledge sources for underwriting and claims, plus the appliance of AI and machine studying.

- Interconnected Tech Foundation — customise the know-how set that may be introduced collectively to satisfy your enterprise technique.

When Majesco checked out weighing progress and innovation, like AM Best scores, we discovered that Leaders by far outpaced Followers and Laggards by way of 5 strategic areas. Are they changing core insurance coverage programs with next-gen cloud core, creating new merchandise, launching new enterprise fashions, increasing distribution channels, and reallocating sources from working the enterprise as is to suit the brand new realities of enterprise? We discovered the hole between Leaders and Followers was about 30% and the hole between Leaders and Laggards was about 70%. And the tempo of change isn’t going to cease. The quicker it continues, the broader the hole can develop into. Interestingly, these gaps line up with AM Best’s first full innovation evaluation for P&C.

Given the macroeconomic shifts, do you see a change in funding priorities? What sorts of refocusing or shifts are you seeing?

Seth Rachlin

It is my notion that insurance coverage corporations sometimes don’t react shortly to altering macroeconomic situations, however they do in the end react. My concern is that the recession, if it will occur or has already begun, will in the end hit know-how budgets. I’m frightened that there will probably be a retrenchment of what’s been a reasonably buoyant tech spending setting inside insurance coverage and that it’s going to in the end decelerate developments which are already shifting not as quick as they need to.

From a precedence perspective, the belongings you outlined are spot on. I don’t assume we’ll see a shifting of priorities. There could also be some heightening of efforts to take price out as a result of powerful financial occasions often convey with them a deal with price. My concern is that the recession slows us all down from the place we should be.

Is Talent additionally a difficulty concerning innovation and focus?

Denise Garth

The U.S. Bureau of Labor Statistics has indicated that the insurance coverage trade is midway via an enormous 15-year shift the place 50% of the workforce goes to retire by 2028. That is barely 5 years away. I used to be not too long ago in a dialog with an insurer who said that they’re anticipating 40% of their workforce to be eligible for retirement throughout the subsequent three years. This wasn’t constructed into their plan! It provides us one other perspective on priorities and the significance of next-gen know-how changing legacy, but in addition in how know-how may optimize the enterprise processes and redefine sure roles to offer a greater buyer expertise.

Seth Rachlin

It’s attainable that these retirement cliffs that we’re speaking about are impeding change, as a result of it creates a degree of threat aversion amongst executives inside insurance coverage. An government is likely to be retirement, considering, “I know how slowly the industry moves. I’m pretty comfortable not having to feel this [innovation] fire under me because I’ll make it another five or 10 years before things really have to change.”

And, I believe that’s completely the mistaken mind-set. The trade has been at this a very long time. We do not make the progress that we have to make. The undeniable fact that AM Best was solely capable of determine just a few leaders, up to now, is indicative of that lack of progress.

I used to be struck with a comparability between this and one thing that Jamie Dimon, the CEO of JPMorgan Chase, stated on the finish of final 12 months after they launched their investor assertion. He stated JPMorgan Chase goes to take a position $12 billion a 12 months in know-how — 10% of their whole income. This represented a 26% improve from the prior 12 months.

When buyers pushed him and requested, “How are you going to measure the return?” he stated, “We’re in this game for the long haul, and we’re in this game to preserve the business and the position that we have. I’m not going to get hung up on measuring ROI quarterly.”

I’ve been round insurance coverage tech a very long time and I’ve by no means seen something like a 26% price range improve. I want that there have been extra folks within the insurance coverage trade who had that degree of braveness. I believe that degree of braveness is what we’d like.

Denise Garth

This factors to a possibility for next-gen cloud know-how funding — a possible benefit that mutual insurers might need over publicly traded insurers. Both are sitting on numerous capital, as a result of they need to from a regulatory standpoint, however there may be nonetheless some huge cash that’s out there for funding. Instead of investing available in the market, possibly these corporations ought to put money into their very own companies.

In our subsequent section, we’ll talk about mutual insurers and their deployment of capital. We will take a look at how innovation is virtually working itself out amongst all completely different traces of enterprise, resembling well being, life, P&C, and among the many completely different supporting gamers inside MGAs and reinsurance. We may even join the dots between the know-how designed to assist insurers forestall and defend and the improvements which are essential inside core programs.

For a preview, make sure you watch Insurance Transformation — Operationally and Strategically — Where are We?

[ad_2]