{kind=link}

[ad_1]

Time-series forecasting is a crucial analysis space that’s vital to a number of scientific and industrial purposes, like retail provide chain optimization, power and visitors prediction, and climate forecasting. In retail use instances, for instance, it has been noticed that enhancing demand forecasting accuracy can meaningfully cut back stock prices and improve income.

Modern time-series purposes can contain forecasting lots of of 1000’s of correlated time-series (e.g., calls for of various merchandise for a retailer) over lengthy horizons (e.g., 1 / 4 or yr away at day by day granularity). As such, time-series forecasting fashions have to fulfill the next key criterias:

- Ability to deal with auxiliary options or covariates: Most use-cases can profit tremendously from successfully utilizing covariates, as an example, in retail forecasting, holidays and product particular attributes or promotions can have an effect on demand.

- Suitable for various information modalities: It ought to have the ability to deal with sparse rely information, e.g., intermittent demand for a product with low quantity of gross sales whereas additionally having the ability to mannequin sturdy steady seasonal patterns in visitors forecasting.

Plenty of neural community–based mostly options have been capable of present good efficiency on benchmarks and in addition help the above criterion. However, these strategies are sometimes sluggish to coach and could be costly for inference, particularly for longer horizons.

In “Long-term Forecasting with TiDE: Time-series Dense Encoder”, we current an all multilayer perceptron (MLP) encoder-decoder structure for time-series forecasting that achieves superior efficiency on lengthy horizon time-series forecasting benchmarks when in comparison with transformer-based options, whereas being 5–10x quicker. Then in “On the benefits of maximum likelihood estimation for Regression and Forecasting”, we reveal that utilizing a fastidiously designed coaching loss operate based mostly on most probability estimation (MLE) could be efficient in dealing with totally different information modalities. These two works are complementary and could be utilized as part of the identical mannequin. In truth, they are going to be out there quickly in Google Cloud AI’s Vertex AutoML Forecasting.

TiDE: A easy MLP structure for quick and correct forecasting

Deep studying has proven promise in time-series forecasting, outperforming conventional statistical strategies, particularly for giant multivariate datasets. After the success of transformers in pure language processing (NLP), there have been a number of works evaluating variants of the Transformer structure for lengthy horizon (the period of time into the longer term) forecasting, similar to FEDformer and PatchTST. However, different work has advised that even linear fashions can outperform these transformer variants on time-series benchmarks. Nonetheless, easy linear fashions will not be expressive sufficient to deal with auxiliary options (e.g., vacation options and promotions for retail demand forecasting) and non-linear dependencies on the previous.

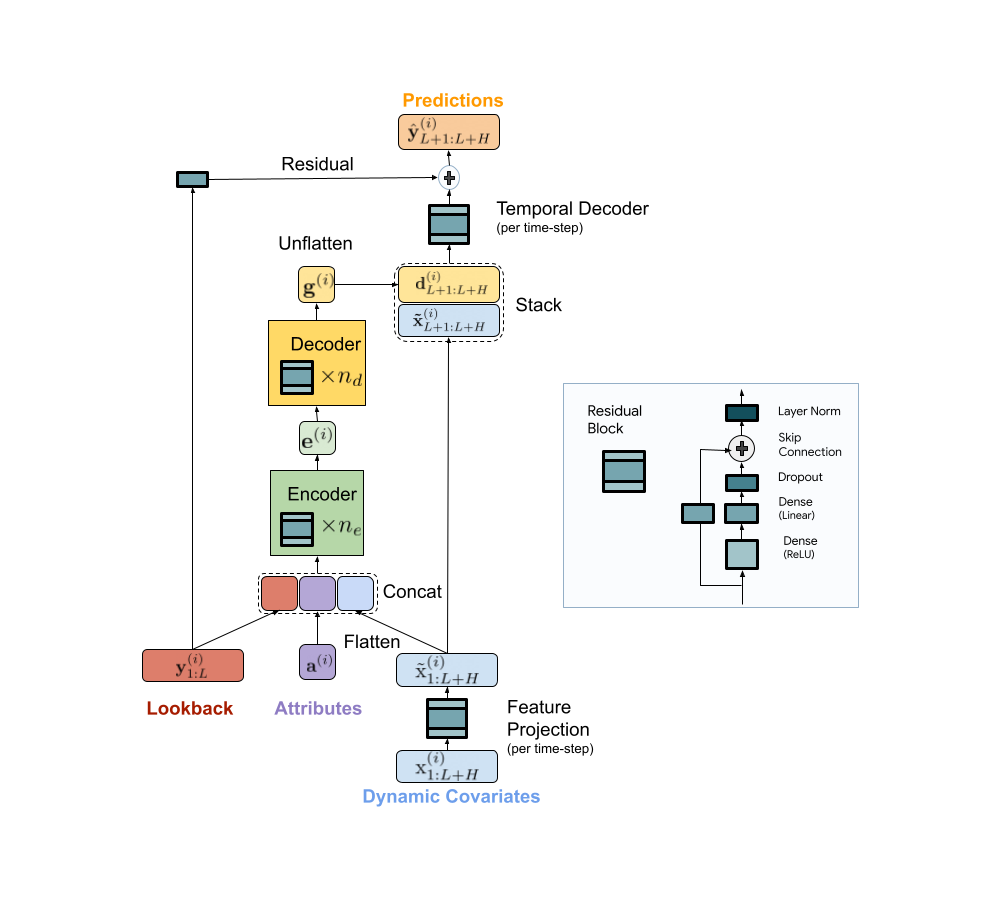

We current a scalable MLP-based encoder-decoder mannequin for quick and correct multi-step forecasting. Our mannequin encodes the previous of a time-series and all out there options utilizing an MLP encoder. Subsequently, the encoding is mixed with future options utilizing an MLP decoder to yield future predictions. The structure is illustrated beneath.

|

| TiDE mannequin structure for multi-step forecasting. |

TiDE is greater than 10x quicker in coaching in comparison with transformer-based baselines whereas being extra correct on benchmarks. Similar good points could be noticed in inference because it solely scales linearly with the size of the context (the variety of time-steps the mannequin seems to be again) and the prediction horizon. Below on the left, we present that our mannequin could be 10.6% higher than one of the best transformer-based baseline (PatchTST) on a preferred visitors forecasting benchmark, when it comes to check imply squared error (MSE). On the suitable, we present that on the similar time our mannequin can have a lot quicker inference latency than PatchTST.

|

| Left: MSE on the check set of a preferred visitors forecasting benchmark. Right: inference time of TiDE and PatchTST as a operate of the look-back size. |

Our analysis demonstrates that we are able to benefit from MLP’s linear computational scaling with look-back and horizon sizes with out sacrificing accuracy, whereas transformers scale quadratically on this state of affairs.

Probabilistic loss capabilities

In most forecasting purposes the top consumer is concerned about in style goal metrics just like the imply absolute share error (MAPE), weighted absolute share error (WAPE), and so forth. In such situations, the usual strategy is to make use of the identical goal metric because the loss operate whereas coaching. In “On the benefits of maximum likelihood estimation for Regression and Forecasting”, accepted at ICLR, we present that this strategy may not at all times be one of the best. Instead, we advocate utilizing the utmost probability loss for a fastidiously chosen household of distributions (mentioned extra beneath) that may seize inductive biases of the dataset throughout coaching. In different phrases, as a substitute of straight outputting level predictions that decrease the goal metric, the forecasting neural community predicts the parameters of a distribution within the chosen household that greatest explains the goal information. At inference time, we are able to predict the statistic from the discovered predictive distribution that minimizes the goal metric of curiosity (e.g., the imply minimizes the MSE goal metric whereas the median minimizes the WAPE). Further, we are able to additionally simply receive uncertainty estimates of our forecasts, i.e., we are able to present quantile forecasts by estimating the quantiles of the predictive distribution. In a number of use instances, correct quantiles are very important, as an example, in demand forecasting a retailer may need to inventory for the ninetieth percentile to protect in opposition to worst-case situations and keep away from misplaced income.

The alternative of the distribution household is essential in such instances. For instance, within the context of sparse rely information, we’d need to have a distribution household that may put extra likelihood on zero, which is usually referred to as zero-inflation. We suggest a mix of various distributions with discovered combination weights that may adapt to totally different information modalities. In the paper, we present that utilizing a mix of zero and a number of unfavorable binomial distributions works nicely in quite a lot of settings as it could actually adapt to sparsity, a number of modalities, rely information, and information with sub-exponential tails.

|

| A mix of zero and two unfavorable binomial distributions. The weights of the three elements, a1, a2 and a3, could be discovered throughout coaching. |

We use this loss operate for coaching Vertex AutoML fashions on the M5 forecasting competitors dataset and present that this straightforward change can result in a 6% acquire and outperform different benchmarks within the competitors metric, weighted root imply squared scaled error (WRMSSE).

| M5 Forecasting | WRMSSE |

| Vertex AutoML | 0.639 +/- 0.007 |

| Vertex AutoML with probabilistic loss | 0.581 +/- 0.007 |

| DeepAR | 0.789 +/- 0.025 |

| FEDFormer | 0.804 +/- 0.033 |

Conclusion

We have proven how TiDE, along with probabilistic loss capabilities, allows quick and correct forecasting that robotically adapts to totally different information distributions and modalities and in addition supplies uncertainty estimates for its predictions. It supplies state-of-the-art accuracy amongst neural community–based mostly options at a fraction of the price of earlier transformer-based forecasting architectures, for large-scale enterprise forecasting purposes. We hope this work can even spur curiosity in revisiting (each theoretically and empirically) MLP-based deep time-series forecasting fashions.

Acknowledgements

This work is the results of a collaboration between a number of people throughout Google Research and Google Cloud, together with (in alphabetical order): Pranjal Awasthi, Dawei Jia, Weihao Kong, Andrew Leach, Shaan Mathur, Petros Mol, Shuxin Nie, Ananda Theertha Suresh, and Rose Yu.

[ad_2]