{kind=link}

[ad_1]

Unfortunately, the excessive value of long-term care providers can simply exhaust an individual’s retirement financial savings. This is why trade consultants suggest taking out long-term care insurance coverage for individuals who can afford to. Apart from serving to seniors shield their retirement fund, the sort of protection offers them the choice to get the very best care attainable.

If you’re an insurance coverage dealer with folks asking questions on long-term care insurance coverage, this is a superb article to share with them.

The reply to this could range from state to state and nation to nation however within the USA, the policyholder must get certification from a good healthcare supplier that they will now not carry out at the very least two of the next actions with out direct help. These are additionally known as “benefit triggers,” And most nations have some type of this:

- Bathing: The means to get out and in of toilet to wash oneself.

- Continence: The means to regulate urinary and bowel actions.

- Dressing: This is the flexibility to placed on or take off one’s personal garments.

- Eating: This is the flexibility to feed oneself.

- Toileting: This is the flexibility to get on and off the bathroom.

- Transferring: This is the flexibility to get out and in of a mattress or a chair.

Policyholders may additionally be eligible for long-term care advantages if they’ve a debilitating situation, together with Alzheimer’s illness, dementia, and schizophrenia.

In addition, most insurance policies require beneficiaries to pay for care providers out of pocket for a sure timeframe, additionally known as an “elimination period.” This normally lasts 30-90 days, after which the insurance coverage supplier begins the reimbursements. LTCI plans pay out as much as a day by day restrict for care till the lifetime most is reached.

Some insurers provide married {couples} a shared care possibility, permitting them to share the whole protection quantity and draw from one another’s pool of advantages as soon as one of many spouses reaches the restrict on their coverage.

Read extra: Top medical insurance suppliers for self-employed Americans

Just like different forms of insurance coverage insurance policies, premiums for long-term care insurance coverage are influenced by a variety of things. These embrace:

- Age: Individuals who take out insurance policies whereas they’re youthful can count on to entry decrease charges, though they must pay their plans longer.

- Health standing: Putting off shopping for insurance coverage till well being issues come up can lead to costlier premiums, or worse, having protection denied.

- Gender: Women usually pay greater than their male counterparts as they have a tendency to have longer lifespans, growing the probability of them making a declare.

- Marital standing: Married {couples} usually get decrease premiums than single people. They even have the choice of buying shared advantages.

- Level of protection: Higher day by day and lifelong limits, in addition to availing of further options – together with inflation safety and shorter elimination durations – can elevate insurance coverage prices.

- Insurer: Rates range between insurance coverage suppliers.

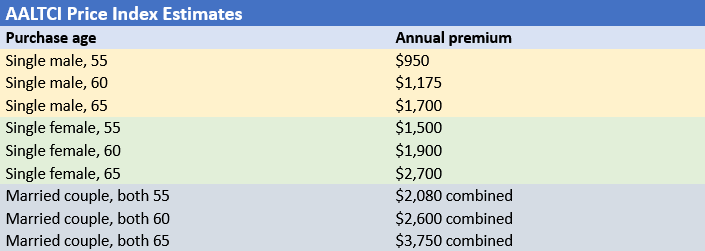

The American Association for Long-Term Care Insurance (AALTCI) lately launched its 2022 Price Index detailing how a lot policyholders of various ages, gender, and marital standing can count on to pay in annual premiums. Here’s a abstract of the prices for a coverage with $165,000 price of protection. According to the trade physique, the charges proven under are for “Select” well being insurance policies, that are costlier than “Preferred” well being plans.

Because such insurance policies present health-related protection, it’s simple to confuse long-term care insurance coverage insurance policies with different types of well being plans. However, there’s a huge distinction when it comes to protection.

- Standard medical insurance: This covers the price of medical therapy, together with medical doctors and hospital visits, emergency surgical procedures, and drugs. It doesn’t cowl long-term care providers.

- Critical sickness insurance coverage: This covers therapy and restoration prices ensuing from extreme diseases. Most insurance policies pay out a lump sum that the policyholder can use to interchange misplaced wages or pay for treatment-related prices and non-medical bills, together with mortgages and groceries.

- Disability insurance coverage: This pays out a portion of revenue if the policyholder is unable to work as a result of damage or sickness.

- Life insurance coverage: This sort of plan works by offering a tax-free lump-sum cost to the policyholder’s household after they die.

- Medicare: Available to seniors and disabled people, Medicare presents restricted advantages for nursing house stays following hospitalization, usually offering cowl provided that the sickness is acute or momentary. It doesn’t cowl long-term custodial care or persistent medical situations.

- Medicaid: This public well being program supplies monetary help for long-term situations, however with strict eligibility standards. Depending on the state, particular revenue limits – $18,745 for states with expanded Medicaid, for instance – are set and beneficiaries could have to liquidate their property or spend a portion of their advantages out of pocket by way of the Medicaid spend-down program to qualify.

Read extra: A information to discovering the very best inexpensive medical insurance plan

The Internal Revenue Service (IRS) permits certified taxpayers to deduct part of their long-term care insurance coverage premiums on their tax returns as “unreimbursed medical expenses,” relying on their age. But they need to itemize these deductions, which should additionally not exceed the adjusted gross revenue (AGI) threshold.

The desk under reveals the 2022 deduction limits set by the statutory physique.

It can be vital to notice that LTCI plans include tax-free advantages, that means policyholders should not taxed from any advantages they obtain.

There are going to be a wide range of insurance policies out there from completely different corporations in your nation, however listed below are the frequent issues to contemplate when selecting your coverage:

- Benefit quantity: This includes assessing the kind of care one expects to obtain and the way a lot it prices each day. One vital factor to be aware of is long-term care bills can range considerably relying on the place an individual lives and the standard of care. Care from a non-public nursing facility, for instance, prices greater than at-home care.

- Payment time period size: Some insurers give clients the choice to decide on how lengthy they wish to pay for the coverage, normally from two years to a lifetime. One main figuring out issue right here is medical historical past. If an individual has a household historical past of a debilitating sickness that may require a few years of care, it might be preferable to choose an extended profit interval.

- Age: Most trade consultants suggest taking out a coverage between your mid-50s and early 60s. Buying an LTCI coverage at a youthful age can assist slash premiums.

- Waiting or elimination interval: Insurers usually impose ready durations of 30, 60, or 90 days earlier than the advantages kick in. This entails policyholders to pay for medical bills out of pocket for a sure interval. One factor to notice is that the longer the elimination interval, the decrease the premiums.

- Inflation safety: Medical bills have soared up to now a number of years as a result of inflation. Nursing house charges, as an illustration, have risen a median of 5% yearly. Insurance suppliers usually provide riders to guard towards inflation, which lead to yearly will increase within the day by day profit.

- Tax implications: Most insurers provide tax-qualified insurance policies, which include tax-free advantages and deductible premiums. The deductions, nevertheless, range relying on the taxpayer’s age.

- Insurer repute: With many suppliers exiting the market in recent times, it is crucial for purchasers to observe due diligence and decide an insurer that’s each financially steady and dedicated to providing policyholders the very best care attainable.

Read extra: Can you utilize life insurance coverage to construct wealth?

The greatest long-term care insurance coverage suppliers are going to range wildly relying on which nation you’re in. Head on over to our Best of Insurance web page and click on in your nation alongside the highest to search for insurance coverage brokerages that can give you the results you want. They are all vetted by their friends in a survey performed by our employees.

What about you? Do you suppose long-term care insurance coverage is price contemplating? Share your ideas within the remark part under.

[ad_2]