{kind=link}

[ad_1]

Identity thieves have been exploiting a evident safety weak spot within the web site of Experian, one of many massive three client credit score reporting bureaus. Normally, Experian requires that these looking for a replica of their credit score report efficiently reply a number of a number of alternative questions on their monetary historical past. But till the tip of 2022, Experian’s web site allowed anybody to bypass these questions and go straight to the buyer’s report. All that was wanted was the individual’s identify, deal with, birthday and Social Security quantity.

The vulnerability in Experian’s web site was exploitable after one utilized to see their credit score file through annualcreditreport.com.

In December, KrebsOnSecurity heard from Jenya Kushnir, a safety researcher residing in Ukraine who stated he found the strategy being utilized by identification thieves after spending time on Telegram chat channels devoted to the cashing out of compromised identities.

“I want to try and help to put a stop to it and make it more difficult for [ID thieves] to access, since [Experian is] not doing shit and regular people struggle,” Kushnir wrote in an e-mail to KrebsOnSecurity explaining his motivations for reaching out. “If somehow I can make small change and help to improve this, inside myself I can feel that I did something that actually matters and helped others.”

Kushnir stated the crooks discovered they may trick Experian into giving them entry to anybody’s credit score report, simply by modifying the deal with displayed within the browser URL bar at a particular level in Experian’s identification verification course of.

Following Kushnir’s directions, I sought a replica of my credit score report from Experian through annualcreditreport.com — a web site that’s required to offer all Americans with a free copy of their credit score report from every of the three main reporting bureaus, as soon as per yr.

Annualcreditreport.com begins by asking to your identify, deal with, SSN and birthday. After I equipped that and instructed Annualcreditreport.com I needed my report from Experian, I used to be taken to Experian.com to finish the identification verification course of.

Normally at this level, Experian’s web site would current 4 or 5 multiple-guess questions, akin to “Which of the following addresses have you lived at?”

Kushnir instructed me that when the questions web page hundreds, you merely change the final a part of the URL from “/acr/oow/” to “/acr/report,” and the location would show the buyer’s full credit score report.

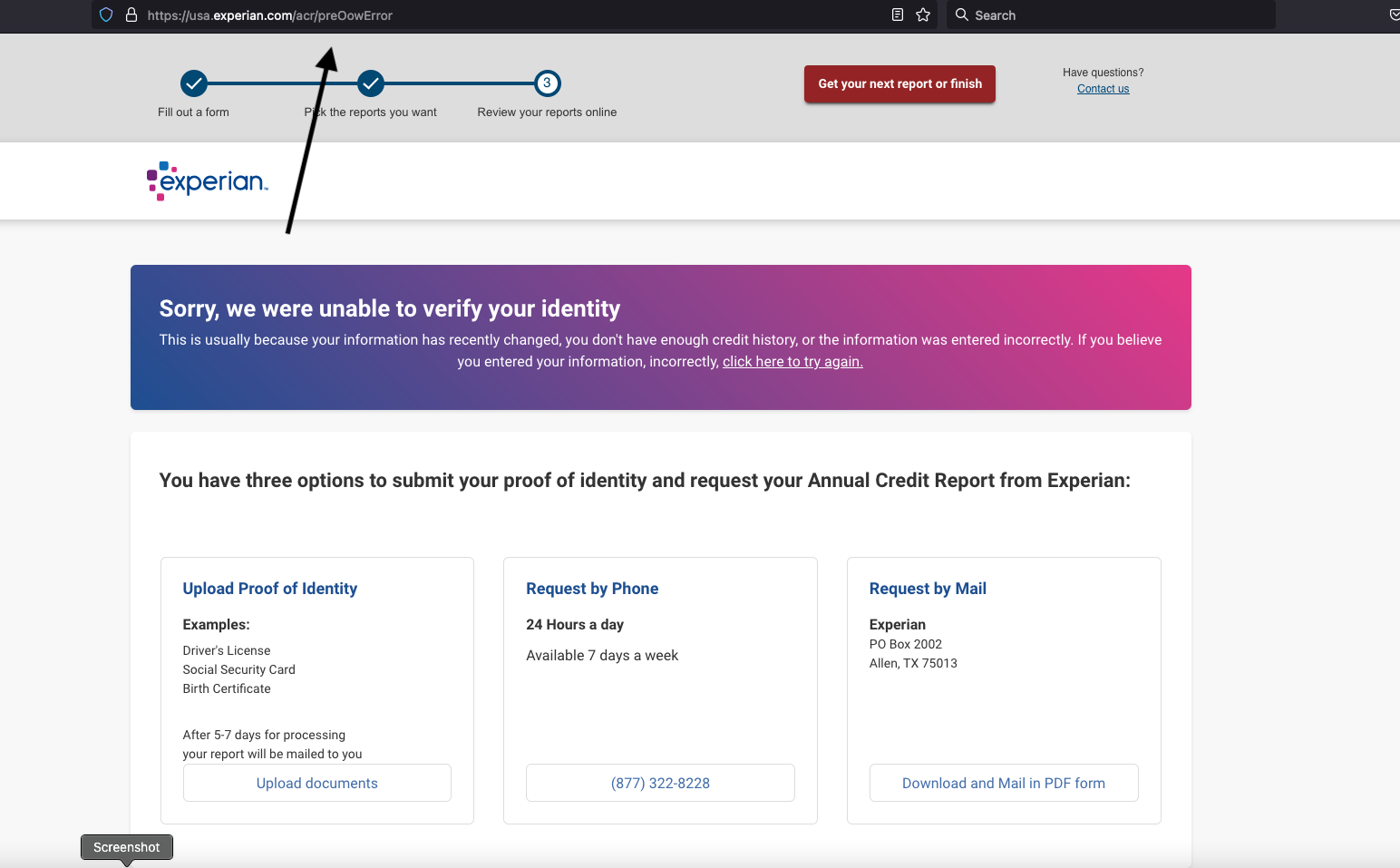

But once I tried to get my report from Experian through annualcreditreport.com, Experian’s web site stated it didn’t have sufficient info to validate my identification. It wouldn’t even present me the 4 multiple-guess questions. Experian stated I had three choices for a free credit score report at this level: Mail a request together with identification paperwork, name a cellphone quantity for Experian, or add proof of identification through the web site.

But that didn’t cease Experian from displaying me my full credit score report after I modified the Experian URL as Kushnir had instructed — modifying the error web page’s trailing URL from “/acr/OcwError” to easily “/acr/report”.

Experian’s web site then instantly displayed my whole credit score file.

Even although Experian stated it couldn’t inform that I used to be truly me, it nonetheless coughed up my report. And thank goodness it did. The report comprises so many errors that it’s most likely going to take a great deal of effort on my half to straighten out.

Now I do know why Experian has NEVER let me view my very own file through their web site. For instance, there have been 4 cellphone numbers on my Experian credit score file: Only one in all them was mine, and that one hasn’t been mine for ages.

I used to be so dumbfounded by Experian’s incompetence that I requested a detailed buddy and trusted safety supply to strive the strategy on her identification file at Experian. Sure sufficient, when she bought to the half the place Experian requested questions, altering the final a part of the URL in her deal with bar to “/report” bypassed the questions and instantly displayed her full credit score report. Her report additionally was replete with errors.

KrebsOnSecurity shared Kushnir’s findings with Experian on Dec. 23, 2022. On Dec. 27, 2022, Experian’s PR crew acknowledged receipt of my Dec. 23 notification, however the firm has to this point ignored a number of requests for remark or clarification.

By the time Experian confirmed receipt of my report, the “exploit” Kushnir stated he discovered from the identification thieves on Telegram had been patched and not labored. But it stays unclear how lengthy Experian’s web site was making it really easy to entry anybody’s credit score report.

In response to info shared by KrebsOnSecurity, Senator Ron Wyden (D-Ore.) stated he was upset — however in no way stunned — to listen to about one more cybersecurity lapse at Experian.

“The credit bureaus are poorly regulated, act as if they are above the law and have thumbed their noses at Congressional oversight,” Wyden stated in a written assertion. “Just last year, Experian ignored repeated briefing requests from my office after you revealed another cybersecurity lapse the company.”

Sen. Wyden’s quote above references a narrative printed right here in July 2022, which broke the information that identification thieves had been hijacking client accounts at Experian.com simply by signing up as them at Experian as soon as extra, supplying the goal’s static, private info (identify, DoB/SSN, deal with) however a unique e-mail deal with.

From interviews with a number of victims who contacted KrebsOnSecurity after that story, it emerged that Experian’s personal buyer help representatives had been truly telling customers who bought locked out of their Experian accounts to recreate their accounts utilizing their private info and a brand new e-mail deal with. This was Experian’s recommendation even for individuals who’d simply defined that this technique was what identification thieves had used to lock them in out within the first place.

Clearly, Experian discovered it less complicated to reply this fashion, fairly than acknowledging the issue and addressing the basis causes (lazy authentication and abhorrent account restoration practices). It’s additionally price mentioning that stories of hijacked Experian.com accounts persevered into late 2022. That screw-up has since prompted a category motion lawsuit towards Experian.

Sen. Wyden stated the Federal Trade Commission (FTC) and Consumer Financial Protection Bureau (CFPB) have to do way more to guard Americans from screw-ups by the credit score bureaus.

“If they don’t believe they have the authority to do so, they should endorse legislation like my Mind Your Own Business Act, which gives the FTC power to set tough mandatory cybersecurity standards for companies like Experian,” Wyden stated.

Sadly, none of that is terribly surprising habits for Experian, which has proven itself a very negligent custodian of obscene quantities of extremely delicate client info.

In April 2021, KrebsOnSecurity revealed how identification thieves had been exploiting lax authentication on Experian’s PIN retrieval web page to unfreeze client credit score recordsdata. In these instances, Experian didn’t ship any discover through e-mail when a freeze PIN was retrieved, nor did it require the PIN to be despatched to an e-mail deal with already related to the buyer’s account.

A couple of days after that April 2021 story, KrebsOnSecurity broke the information that an Experian API was exposing the credit score scores of most Americans.

It’s dangerous sufficient that we will’t actually decide out of corporations like Experian making $2.6 billion every quarter accumulating and promoting gobs of our private and monetary info. But there must be some significant accountability when these monopolistic corporations have interaction in negligent and reckless habits with the exact same client knowledge that feeds their quarterly earnings. Or when safety and privateness shortcuts are discovered to be intentional, like for cost-saving causes.

And as we noticed with Equifax’s consolidated class-action settlement in response to letting state-sponsored hackers from China steal knowledge on practically 150 million Americans again in 2017, class-actions and extra laughable “free credit monitoring” providers from the exact same corporations that created the issue aren’t going to chop it.

WHAT CAN YOU DO?

It is straightforward to undertake a defeatist perspective with the credit score bureaus, who typically foul issues up royally even for customers who’re fairly diligent about watching their client credit score recordsdata and disputing any inaccuracies.

But there are some concrete steps that everybody can take which can dramatically decrease the danger that identification thieves will smash your monetary future. And fortunately, most of those steps have the facet good thing about costing the credit score bureaus cash, or not less than inflicting the info they acquire about you to develop into much less priceless over time.

The first step is consciousness. Find out what these corporations are saying about you behind your again. Keep in thoughts that — truthful or not — your credit score rating as collectively decided by these bureaus can have an effect on whether or not you get that mortgage, condo, or job. In that context, even small, unintentional errors which can be unrelated to identification theft can have outsized penalties for customers down the street.

Each bureau is required to offer a free copy of your credit score report yearly. The best approach to get yours is thru annualcreditreport.com.

Some customers report that this web site by no means works for them, and that every bureau will insist they don’t have sufficient info to offer a report. I’m undoubtedly on this camp. Thankfully, a monetary establishment that I have already got a relationship with gives the power to view your credit score file by way of them. Your mileage on this entrance could differ, and it’s possible you’ll find yourself having to ship copies of your identification paperwork by way of the mail or web site.

When you get your report, search for something that isn’t yours, after which doc and file a dispute with the corresponding credit score bureau. And after you’ve reviewed your report, set a calendar reminder to recur each 4 months, reminding you it’s time to get one other free copy of your credit score file.

If you haven’t already performed so, take into account making 2023 the yr that you just freeze your credit score recordsdata on the three main reporting bureaus, together with Experian, Equifax and TransUnion. It is now free to individuals in all 50 U.S. states to position a safety freeze on their credit score recordsdata. It can be free to do that to your accomplice and/or your dependents.

Freezing your credit score means nobody who doesn’t have already got a monetary relationship with you possibly can view your credit score file, making it unlikely that potential collectors will grant new strains of credit score in your identify to identification thieves. Freezing your credit score file additionally means Experian and its brethren can not promote peeks at your credit score historical past to others.

Anytime you want to apply for brand new credit score or a brand new job, or open an account at a utility or communications supplier, you possibly can shortly thaw a freeze in your credit score file, and set it to freeze routinely once more after a specified size of time.

Please don’t confuse a credit score freeze (a.okay.a. “security freeze”) with the choice that the bureaus will possible steer you in direction of while you ask for a freeze: “Credit lock” providers.

The bureaus pitch these credit score lock providers as a manner for customers to simply toggle their credit score file availability with push of a button on a cell app, however they do little to stop the bureaus from persevering with to promote your info to others.

My recommendation: Ignore the lock providers, and simply freeze your credit score recordsdata already.

One ultimate notice. Frequent readers right here may have observed that I’ve criticized these so-called “knowledge-based authentication” or KBA questions that Experian’s web site didn’t ask as a part of its client verification course of.

KrebsOnSecurity has lengthy assailed KBA as weak authentication as a result of the questions and solutions are drawn largely from client data which can be public and simply accessible to organized identification theft teams.

That stated, on condition that these KBA questions seem like the ONLY factor standing between me and my Experian credit score report, it looks as if perhaps they need to not less than take care to make sure that these questions truly get requested.

[ad_2]