{kind=link}

[ad_1]

Many small companies and startups function on restricted monetary sources, so it may be tempting for them to typically skip sure coverages, particularly if these will not be mandated by the legislation.

But these enterprises additionally typically face many conditions that require them to take a leap of religion. While such circumstances current thrilling alternatives for development, they’ll additionally expose companies to sudden dangers – and when these dangers do occur, it pays for corporations to have some type of monetary cushion.

Insurance for small companies offers monetary safety from unlucky eventualities that would have in any other case price enterprises hundreds, if not thousands and thousands of {dollars}, making it tough for them to get better. Having the precise insurance policies in place performs a vital position in serving to corporations get again on their toes quicker.

Another good thing about carrying correct protection is that it helps bolster an organization’s status and credibility as prospects typically desire working with companies that they know are protected financially.

Taking out insurance coverage, nevertheless, is only one aspect of how small companies can decrease their losses. Pairing insurance coverage protection with good threat administration practices is among the many finest methods corporations can defend their property and funds.

Because every small enterprise faces a unique set of dangers and challenges, there isn’t any one-size-fits-all small enterprise insurance coverage coverage that may cater to each want. The kind of protection an organization requires relies on an assortment of things, together with the character of the enterprise, the business it operates in, and the variety of workers.

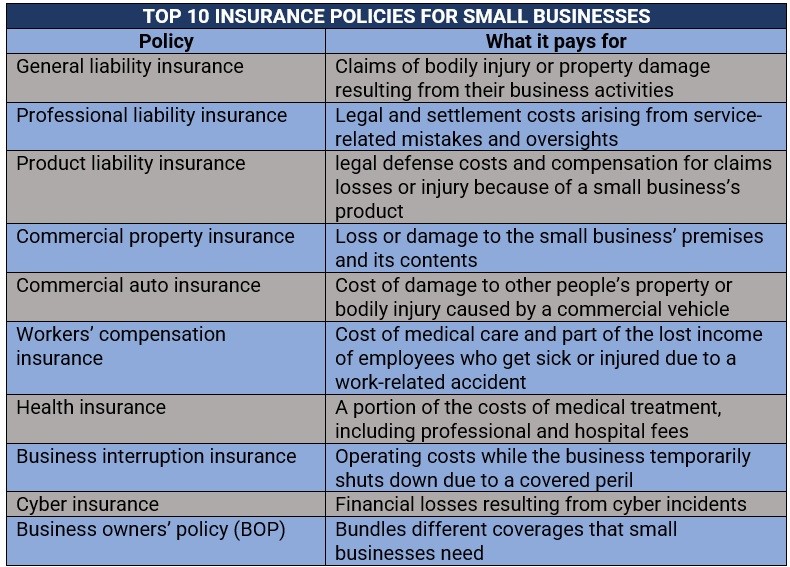

Small enterprise insurance coverage suppliers supply a spread of insurance policies that may assist defend corporations in opposition to the totally different dangers they face. The choice is various, however in line with business specialists, these are among the most important forms of insurance policies that companies want to take care of their operations when accidents and calamities strike.

1. General legal responsibility insurance coverage

General legal responsibility insurance coverage is likely one of the most vital coverages that small enterprises want, in line with the US Small Business Administration (SBA). Sometimes known as enterprise legal responsibility or public legal responsibility protection, it protects corporations in opposition to claims of bodily harm or property harm ensuing from their enterprise actions. Policies additionally present protection for claims of reputational harm, together with libel, slander, and copyright infringement.

Small companies don’t obtain compensation for any such protection, as an alternative the payouts are given to the affected third get together. Without normal legal responsibility insurance coverage, corporations might want to pay for the claims out of pocket.

2. Professional legal responsibility insurance coverage

Professional legal responsibility protection protects small companies from work-related claims. These embrace:

- Inaccurate recommendation

- Misrepresentation

- Negligence

- Personal harm similar to libel or slander

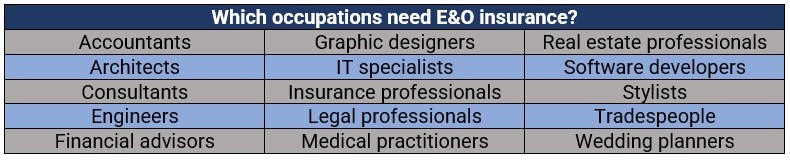

Also known as errors and omissions (E&O) or malpractice insurance coverage, it covers authorized and settlement prices arising from service-related errors and oversights, breach of contract, unfinished work, and finances overruns, amongst others.

Professional legal responsibility insurance coverage covers all of a enterprise’s workers and the corporate itself. Although not all the time legally required, having this type of protection is crucial for a lot of small enterprises, particularly for those who present professional or advisory providers. The checklist consists of:

3. Product legal responsibility insurance coverage

Product legal responsibility protection could also be value contemplating for corporations that promote merchandise. This kind of insurance coverage for small companies protects them in opposition to lawsuits from prospects claiming losses or harm due to the product. It additionally covers authorized protection prices and compensation if the enterprise is discovered to be at fault.

4. Commercial property insurance coverage

Designed to decrease disruption to a small enterprise’s day-to-day operations, industrial property insurance coverage offers compensation for damages or losses that occur to the next:

- Property or constructing the corporate operates in

- Equipment and expertise the small enterprise makes use of

- Inventory of merchandise and supplies the corporate shops and sells

Some insurance policies additionally pay out a portion of misplaced earnings if the harm prevents the enterprise from conducting its regular operations. Also known as enterprise property or industrial constructing insurance coverage, any such protection is usually a requirement in industrial leasing preparations.

5. Commercial auto insurance coverage

Commercial auto insurance coverage is a sort of automotive coverage designed for automobiles pushed for enterprise functions. In phrases of safety, it really works equally to private auto insurance coverage however covers primarily firm automobiles and industrial vans and vans. Coverage usually consists of:

- Bodily harm legal responsibility: Covers accidents the motive force causes one other particular person and authorized charges if they’re sued over the accident.

- Property harm legal responsibility: Pays out if the enterprise’s automobile damages one other particular person’s property and authorized protection prices incurred in a lawsuit.

- Combined single restrict (CSL) legal responsibility: Provides an general restrict for bodily harm and property harm claims in opposition to the enterprise relatively than having two separate limits.

- Personal harm safety (PIP): Covers medical bills for the motive force and the passengers ensuing from accidents coated by the coverage. In the US, PIP is necessary in no-fault insurance coverage states.

- Collision insurance coverage: Pays for harm to the industrial automobile if it collides with one other automotive or object.

- Comprehensive insurance coverage: Provides protection for harm to the industrial automobile, ensuing from hearth, flood, theft, vandalism, and different coated perils.

- Uninsured motorist (UM) protection: Pays out for accidents the motive force and their passengers maintain if they’re hit by an uninsured driver or become involved in a hit-and-run accident.

- Underinsured motorist (UIM) protection: Covers medical bills incurred when the motive force or passengers of a industrial automobile are hit by somebody whose coverage isn’t sufficient to cowl all the prices.

Some states within the US enable industrial automobile drivers to buy UM and UIM protection individually. They can even discover business-specific protection, together with these for misplaced enterprise earnings.

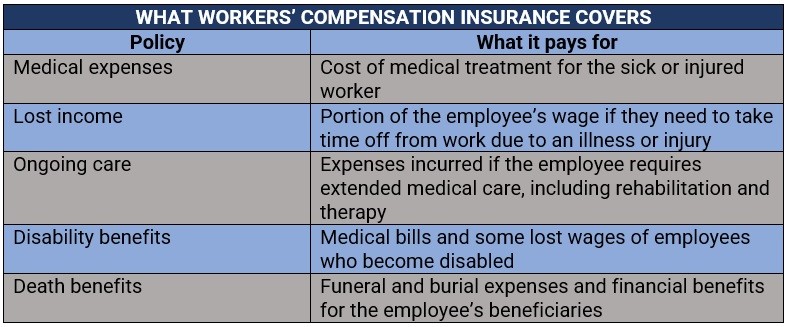

6. Workers’ compensation insurance coverage

Small companies with a minimum of one workers member are required to take out employees’ compensation insurance coverage. This pays out the price of medical care and a part of the misplaced earnings of workers who get sick or injured whereas performing their jobs. It additionally protects small companies from the monetary legal responsibility of getting to pay for bills stemming from work-related diseases and accidents out of pocket.

Workers’ compensation insurance coverage offers several types of safety summarized within the desk beneath.

7. Health insurance coverage

Businesses that make use of greater than 50 full-time workers within the USA are required to take out medical health insurance for his or her employees, in line with the Affordable Care Act (ACA), and most nations have a typical quantity for this. For these with lower than 50 workers, the ACA affords a Small Business Health Options Program (SHOP) as protection.

Health insurance coverage suppliers supply fundamental healthcare protection to small companies, together with different providers that may embrace Medicaid and Medicare insurance policies, long-term care insurance coverage, dental protection, and imaginative and prescient advantages. In the US, the high 10 non-public medical health insurance corporations management nearly two-thirds of the market.

8. Business interruption insurance coverage

Business interruption insurance coverage is designed to guard corporations in opposition to monetary losses incurred from the disruption of their operations ensuing from an insured peril. Also known as BI or enterprise earnings protection, it pays out the working prices whereas the enterprise quickly shuts down. These embrace:

- Potential income

- Mortgage or hire on industrial area

- Business mortgage repayments

- Employee salaries

- Taxes

Some BI insurance policies additionally present protection for added bills associated to the closure similar to the price of organising a short lived location or the coaching of workers to make use of new tools.

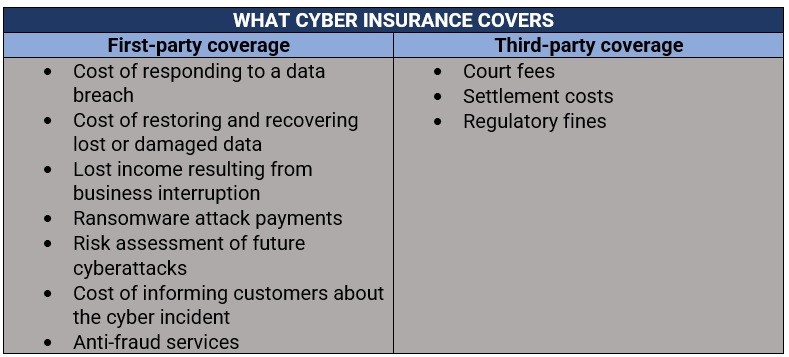

9. Cyber insurance coverage

The goal of cyber insurance coverage is to guard small companies in opposition to monetary losses ensuing from cyber incidents. Policies usually present two forms of safety:

- First-party protection: Pays out for the monetary losses the enterprise incurs as a consequence of a cyber incident.

- Third-party protection: Provides monetary safety in opposition to lawsuits filed by third events – together with prospects, workers, and distributors – for damages attributable to a cyberattack on the enterprise. Here’s a abstract of what these insurance policies cowl.

Learn easy and sensible methods in which you’ll defend your small enterprise in opposition to cyber threats in our cybersecurity information.

10. Business house owners’ coverage (BOP)

Designed for small and mid-size companies, BOP bundles totally different insurance coverage insurance policies that corporations want, together with:

- General legal responsibility insurance coverage

- Commercial property insurance coverage

- Business interruption insurance coverage

- Workers’ compensation insurance coverage

Some insurers enable small companies so as to add protection at a corresponding price relying on their wants. BOP additionally offers a inexpensive various to purchasing totally different enterprise insurance coverage insurance policies individually.

Here’s a abstract of the totally different insurance coverage insurance policies that house owners might need to think about to guard their small companies financially when accidents and disasters happen.

Because the protection supplied by every coverage varies enormously, there’s additionally an enormous distinction between the elements dictating premium costs for every kind of small enterprise insurance coverage.

Rates for skilled legal responsibility protection, for instance, are calculated utilizing the next parameters:

- The business and the dangers related to it

- Where the enterprise is situated

- Coverage limits and deductibles

- Years of operation

- Number of workers

- Past claims

According to information gathered by Insureon, an impartial insurance coverage market for small companies, the median price {of professional} legal responsibility premiums is $59 per 30 days or about $713 yearly. The agency added that greater than half of its small enterprise shoppers allocate between $500 and $1,000 every year for E&O protection. About a fifth spend lower than $500.

For normal legal responsibility protection, prospects pay a median premium of $42 per 30 days, or about $500 yearly, no matter coverage limits.

Commercial property insurance coverage for small companies

Commercial property insurance coverage premiums, in the meantime, are influenced by the next elements:

- Age of the property: Rates for older buildings are greater than these for newer industrial areas because the latter typically incorporate fashionable security options.

- Location: Commercial properties in areas which have had numerous claims are sometimes costly to insure.

- Size of the constructing: Bigger industrial properties usually have greater premiums as these are extra pricey to rebuild and restore.

- Equipment and equipment: Insurance charges for companies utilizing specialised tools are costlier as this can be tough to exchange. For the identical cause, corporations with older, outdated equipment get greater premiums as nicely.

- Safety and safety measures: Having closed-circuit tv (CCTV), monitored alarms, safety patrols, deadlocks, and strengthened entry factors can assist a enterprise deliver down premiums.

- Total worth of contents: Premiums are additionally depending on how a lot tools, fixtures and fittings, furnishings, and inventory inside a industrial property are value.

Workers’ compensation insurance coverage for small companies

For employees’ compensation, the premium determinants embrace:

- The kind of business

- Job classification codes, which may replicate the riskiness of the work workers do

- Experience modification score, which is decided utilizing the corporate’s payroll and previous employees comp claims

- Safety measures carried out within the office

Small companies pay a mean of $47 month-to-month, or about $560 yearly for protection, in line with an estimate by Trusted Choice, a Virginia-based community of insurance coverage brokers and brokers.

Cybersecurity insurance coverage premiums, in the meantime, are decided by the dimensions, nature, and placement of the enterprise. Data gathered by the small enterprise data useful resource web site AdvisorSmith reveals that the typical price of cyber insurance coverage within the US is about $1,589 per yr or $132 per 30 days.

Because of the essential position insurance coverage performs in defending a small enterprise, business specialists advise corporations to buy round and examine choices from a number of suppliers to make it possible for they get the safety they want at the absolute best worth. Here are the important thing standards that specialists say small companies should think about when choosing the proper insurance coverage insurance policies:

- Coverage choices: Many insurance policies look comparable throughout insurers when it comes to which perils will or won’t be coated. Small companies ought to ask their insurance coverage suppliers about including or extending coverages to go well with their enterprise wants.

- Policy limits: Businesses ought to make it possible for the restrict of every insurance coverage coverage can cowl the complete worth of the safety they require.

- Premiums and deductibles: Experts warn small companies in opposition to selecting the most cost effective obtainable coverage, which might price them tens to lots of of hundreds – doubtlessly even thousands and thousands in the long term. Companies ought to search for insurance policies with premiums and deductibles that supply the most effective worth for the quantity of protection and the relative stage of threat going through their companies.

- Claims reporting: Businesses must also make it possible for they’ll navigate the claims course of simply to reduce monetary losses and disruptions to their operations. The course of is usually specified by the product disclosure assertion of the coverage.

- Company status: Businesses ought to search for insurance coverage suppliers with an excellent observe file for buyer satisfaction and honest enterprise practices.

- Financial stability: Companies ought to make it possible for their insurer is in fine condition financially to cowl claims which will come up.

Are you a small enterprise proprietor looking for the precise protection? What insurance policies do you suppose are important for small companies? Share your ideas within the feedback part beneath.

[ad_2]