{kind=link}

[ad_1]

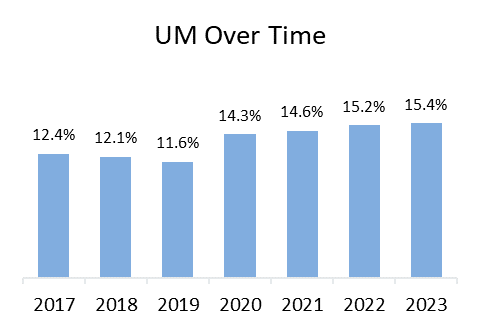

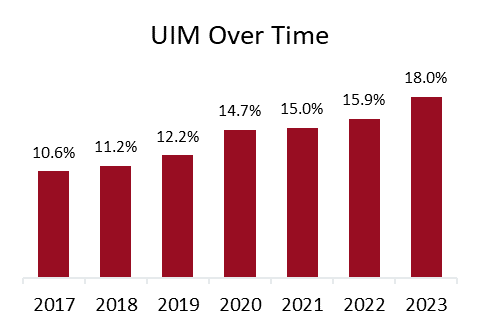

In 2023, regardless of practically common authorized necessities to have auto insurance coverage, multiple in seven drivers (15.4 p.c) nationally had been uninsured, and multiple in six drivers (18.0 p.c) had been underinsured, in keeping with the brand new report, Uninsured and Underinsured Motorists: 2017–2023, by the Insurance Research Council (IRC), affiliated with The Institutes. Across the fifty states and the District of Columbia, one in three drivers (33.4 p.c) had been both uninsured or underinsured in 2023, a ten share level enhance within the mixed fee since 2017.

Using information submitted by 17 insurers — representing roughly 55 p.c of the non-public passenger auto insurance coverage market countrywide — this newest report estimated the prevalence of uninsured (UM) and underinsured (UIM) by evaluating the frequency of UM claims and UIM claims, respectively, to the frequency of bodily harm (BI) claims. Findings included an evaluation of developments and contributing elements to variations in UM and UIM charges throughout states.

The IRC analyzed UM, UIM, and BI legal responsibility publicity and declare rely information from taking part firms for 2017 by 2023. Because of the disruption of the pandemic shutdowns, the modifications over time had been cut up into three intervals (particulars outlined within the report).

Key IRC findings embody:

- UM charges diverse considerably throughout the nation (50 states and the District of Columbia)

- Nearly each state noticed an increase within the UM fee in 2020 with the onset of the pandemic, however the expertise from 2020 to 2023 was blended.

- Every state, aside from New York and the District of Columbia, skilled an increase in UIM fee between 2017 and 2023.

- Many states with excessive UM charges usually even have excessive UIM charges. However, some jurisdictions, reminiscent of Nevada and Louisiana, mix below-average UM charges with excessive UIM charges, whereas others, such because the District of Columbia, have excessive UM charges however low UIM charges.

- Several elements, together with financial elements, insurance coverage prices, and state insurance coverage legal guidelines and rules, are related to variations in UM and UIM charges throughout states.

After the preliminary shock of the pandemic, the UM fee elevated steadily.

Before the disruption of the COVID-19 pandemic, UM charges had been falling in most states. From 2017 to 2019, solely 11 jurisdictions noticed a rise. UM declare frequency fell barely in 2020 to 0.11 claims per 100 insured autos, however the decline was a lot smaller than the drop in BI declare frequency. UM declare frequency recovered rapidly and, within the years since 2020, has grown sooner than BI declare frequency (39 p.c in contrast with 29 p.c).

As a consequence, the UM fee has elevated steadily, reaching 15.4 p.c in 2023. The vary of the UM charges spanned from a low of 5.7 p.c in Maine to a excessive of 28.2 p.c in Mississippi. Outliers embody eight states with UM charges above 20 p.c and 11 states with charges decrease than 10 p.c.

States with above-average BI declare frequency and UM declare frequency tended to have larger UM charges. Yet, some states with low UM declare frequency charges have a comparatively excessive UM fee. In Michigan, for instance, strict no-fault guidelines restrict the variety of BI claims, so the ratio of UM-to-BI declare frequencies is excessive. Lower UM charges tended to happen in states with larger revenue, decrease unemployment charges, decrease insurance coverage expenditures, low minimal limits, and an absence of stacking provisions.

UM charges had been larger in states that don’t require UIM protection. In 2023, the UM fee was 14.9 p.c in states that don’t require UIM insurance coverage, in contrast with 11.6 p.c in states that require it. Where UIM protection isn’t required by regulation, UM charges had been considerably larger within the years captured on this research, with the speed in 2023 at 18.9 p.c in states that don’t require UIM insurance coverage, in contrast with 13.3 p.c in states that require it.

Nearly one in 5 accidents with accidents concerned losses greater than the at-fault driver’s protection limits.

Over the research interval, practically each jurisdiction skilled a rise in its UIM fee. The solely exceptions had been a small decline (0.9%) within the District of Columbia and a 6.6 p.c decline in New York. The largest enhance occurred in Colorado, the place the UIM fee rose 24.4 share factors. Other states with above-average will increase included Michigan, Kentucky, and Georgia.

UIM declare frequency confirmed a small enhance between 2017 and 2019 earlier than dropping barely in 2020. In the years because the onset of the pandemic, with the severity of auto harm claims on the rise, UIM declare frequency has elevated markedly, reaching 0.17 claims per 100 insured autos in 2023. Since 2020, the expansion in UIM declare frequency was double the expansion in BI frequency. As a consequence, the UIM fee has elevated considerably, rising to 18.0 p.c in 2023.

IRC evaluation confirmed that traits related to decrease UIM charges included larger revenue, decrease unemployment charges, decrease insurance coverage expenditures, excessive or medium minimal limits, lack of stacking provisions, and use of a limits set off for UIM protection somewhat than a damages set off. States with excessive UM charges usually even have excessive UIM charges. Florida, Colorado, and Michigan all rank comparatively excessive for each measures, whereas Maine, Massachusetts, and Nebraska all rank comparatively low.

“The increase in UIM rates points to higher UIM premiums in the future, worsening affordability and potentially increasing the likelihood of more uninsured drivers. This demonstrates the complex interconnectedness of these two coverages as insurers protect consumers from insufficient coverage by at-fault drivers,” mentioned Dale Porfilio, president of the IRC and chief insurance coverage officer on the Insurance Information Institute (Triple-I).

While state legal guidelines concerning obligatory necessities for uninsured and underinsured motorists fluctuate, practically all states have a laws framework that requires all drivers to have some auto legal responsibility insurance coverage to drive a motorcar. Drivers in most states are additionally required to buy further safety to supply protection if the at-fault driver can not afford to pay for the harm they induced. However, legislators in a number of states have enacted “no pay, no play” legal guidelines, which ban uninsured drivers from suing for noneconomic damages reminiscent of ache and struggling. A handful of states have packages to help lower-income drivers, and drivers can examine with their state’s insurance coverage division to see if they’re eligible.

To be taught extra about UM/UIM developments, learn the IRC report, Uninsured and Underinsured Motorists: 2017–2023, and take a look at the Triple-I Backgrounder on Compulsory Auto/Uninsured Motorists.

[ad_2]