{kind=link}

[ad_1]

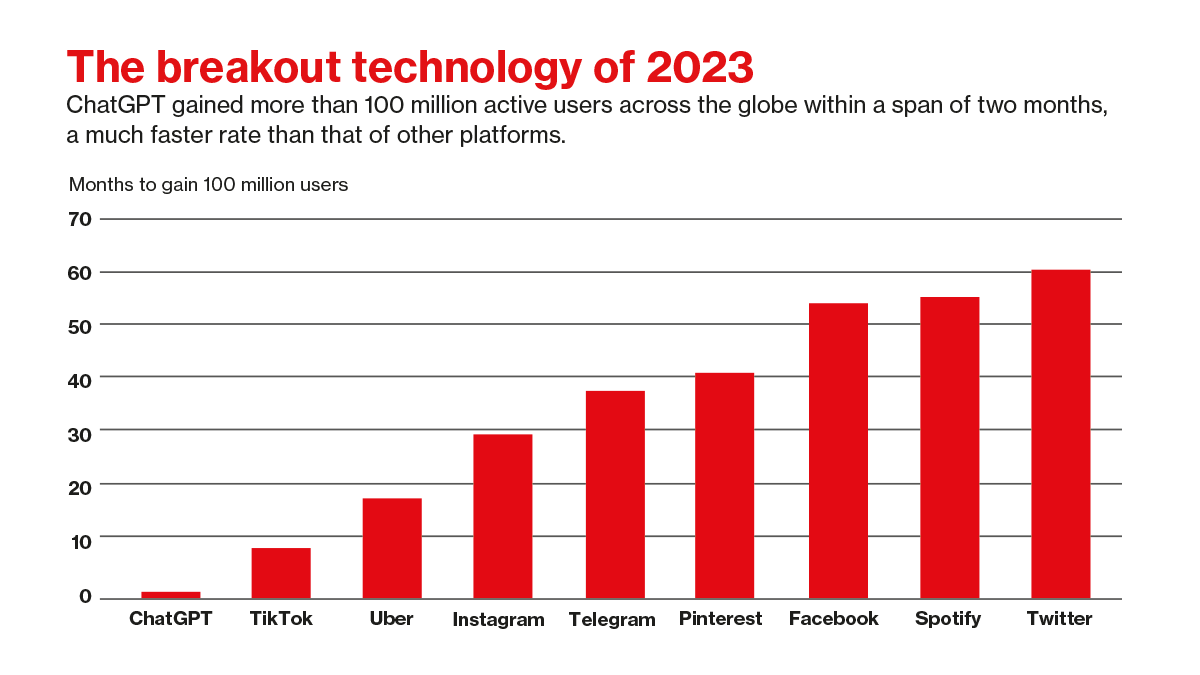

According to a McKinsey report, generative AI might add $2.6 trillion to $4.4 trillion yearly in worth to the worldwide economic system. The banking business was highlighted as amongst sectors that might see the largest impression (as a share of their revenues) from generative AI. The know-how “could deliver value equal to an additional $200 billion to $340 billion annually if the use cases were fully implemented,” says the report.

For companies from each sector, the present problem is to separate the hype that accompanies any new know-how from the true and lasting worth it might convey. This is a urgent concern for corporations in monetary companies. The business’s already in depth—and rising—use of digital instruments makes it significantly prone to be affected by know-how advances. This MIT Technology Review Insights report examines the early impression of generative AI throughout the monetary sector, the place it’s beginning to be utilized, and the limitations that should be overcome in the long term for its profitable deployment.

The primary findings of this report are as follows:

- Corporate deployment of generative AI in monetary companies remains to be largely nascent. The most energetic use instances revolve round reducing prices by liberating staff from low-value, repetitive work. Companies have begun deploying generative AI instruments to automate time-consuming, tedious jobs, which beforehand required people to evaluate unstructured data.

- There is in depth experimentation on doubtlessly extra disruptive instruments, however indicators of economic deployment stay uncommon. Academics and banks are inspecting how generative AI might assist in impactful areas together with asset choice, improved simulations, and higher understanding of asset correlation and tail threat—the chance that the asset performs far under or far above its common previous efficiency. So far, nonetheless, a spread of sensible and regulatory challenges are impeding their business use.

- Legacy know-how and expertise shortages could sluggish adoption of generative AI instruments, however solely briefly. Many monetary companies firms, particularly massive banks and insurers, nonetheless have substantial, growing old data know-how and information constructions, doubtlessly unfit for the usage of trendy purposes. In latest years, nonetheless, the issue has eased with widespread digitalization and should proceed to take action. As is the case with any new know-how, expertise with experience particularly in generative AI is briefly provide throughout the economic system. For now, monetary companies firms seem like coaching employees quite than bidding to recruit from a sparse specialist pool. That mentioned, the problem to find AI expertise is already beginning to ebb, a course of that might mirror these seen with the rise of cloud and different new applied sciences.

- More troublesome to beat could also be weaknesses within the know-how itself and regulatory hurdles to its rollout for sure duties. General, off-the-shelf instruments are unlikely to adequately carry out advanced, particular duties, similar to portfolio evaluation and choice. Companies might want to prepare their very own fashions, a course of that may require substantial time and funding. Once such software program is full, its output could also be problematic. The dangers of bias and lack of accountability in AI are well-known. Finding methods to validate advanced output from generative AI has but to see success. Authorities acknowledge that they should examine the implications of generative AI extra, and traditionally they’ve hardly ever permitted instruments earlier than rollout.

This content material was produced by Insights, the customized content material arm of MIT Technology Review. It was not written by MIT Technology Review’s editorial employees.

[ad_2]