{kind=link}

[ad_1]

In this a part of our consumer schooling sequence, Insurance Business explains what an insurance coverage premium is, the way it works, and the way it’s calculated for various kinds of protection. We encourage insurance coverage brokers and brokers to share this text with their purchasers to offer them a deeper understanding of this significant aspect of an insurance coverage coverage.

An insurance coverage premium is the quantity the policyholder agrees to pay in alternate for protection. It ensures monetary compensation for the damages or losses they incur, so long as well timed funds are made. Depending on the kind of coverage, the insurance coverage firm might require premiums to be paid month-to-month, semi-annually, or yearly.

Policyholders want to satisfy common premium funds to maintain their plans lively. Failure to take action might void their insurance policies and have an effect on their future eligibility for acquiring protection.

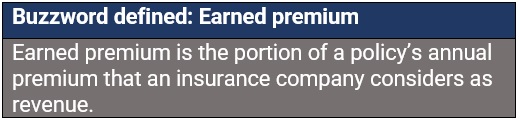

Insurance corporations, in flip, use the premiums they acquire to make sure that they’ve sufficient liquid property to have the ability to present monetary compensation to policyholders in an occasion of a declare. If the amount of cash they safe exceeds what they pay in claims prices and operational bills, the distinction is taken into account revenue, additionally known as earned premium.

Some insurers additionally use premiums as an funding instrument to generate increased returns. This technique permits them to offset a number of the prices related to offering protection and preserve their insurance coverage costs aggressive.

While investing premiums could also be a worthwhile transfer for a lot of insurance coverage suppliers, they’re nonetheless required to keep up a sure degree of liquidity to make sure that they’ve sufficient property to pay for claims. The quantity is about by state insurance coverage regulators.

Insurance premiums may additionally embrace service prices, relying on state insurance coverage legal guidelines and the insurance coverage contract. Any extra prices, nonetheless, have to be itemized individually on the premium or account assertion.

There are a number of components that affect the value of an insurance coverage premium, however typically, it’s primarily based on the policyholder’s threat degree. This implies that the extra dangers they pose to the insurer, the upper their premiums will probably be.

Depending on the kind of protection, insurance coverage corporations use totally different parameters in calculating premiums.

Auto insurance coverage

Different automobile insurance coverage suppliers use totally different metrics in figuring out how a lot threat a motorist poses to them. These embrace driving-related components corresponding to visitors violations and sort of car, which carry an enormous weight in calculating premiums, and private attributes, together with gender and marital standing, that are thought of not as important.

Here are a number of the most widespread components auto insurers take into accounts when figuring out insurance coverage charges, in keeping with the Insurance Information Institute (Triple-I).

- Driving file: Auto insurers view a poor driving file as a sign {that a} motorist is extra more likely to file a declare sooner or later. As a end result, at-fault accidents can drive up charges significantly.

- Mileage: The extra an individual drives, the upper the chance that they might get into an accident, which might increase insurance coverage premiums.

- Residence: Policyholders who stay in areas with excessive charges of crime and accidents will possible pay increased premiums than those that reside in safer places.

- Vehicle sort: How a lot a automobile prices, how costly it’s to restore, how highly effective the engine, its security options, and the way inclined it’s to theft are among the many components which have a significant impression on automobile insurance coverage premiums.

- Age: Because an individual’s age correlates with driving expertise and the chance of getting concerned in an accident, younger drivers usually pay the best auto insurance coverage charges.

- Gender: Statistically, male drivers usually tend to get entangled in accidents than feminine motorists, pushing up the premiums they should pay.

- Credit ranking: Car insurance coverage corporations in most states use credit-based insurance coverage scores to assist decide premiums as these suppliers usually imagine that policyholders with excessive scores are likely to file fewer claims than these with decrease credit score scores.

- Level of protection: Comprehensive insurance policies require increased premiums than primary plans however provide broader safety.

Home insurance coverage

Home insurers think about a spread of parameters when figuring out premiums, the largest of that are the house’s location and the price of a rebuild. Here’s how these and different components impression the price of house insurance coverage premiums.

- Address: The premiums for properties in disaster-prone and high-crime areas are increased in comparison with these in safer neighborhoods. To decide by which sort of space a house is positioned, insurers usually observe the amount, sorts, and value of claims in every zip code.

- Rebuilding price: Higher-priced properties price extra to insure as they’re additionally dearer to rebuild or restore. Most insurance coverage corporations use an insurance-to-value evaluator to calculate rebuilding prices primarily based on a number of components, together with the home’s building, sq. footage, and the variety of flooring.

- The house’s age: Older and classic homes have increased insurance coverage prices as these usually have options and building supplies which might be expensive and troublesome to switch.

- The house’s claims historical past: If owners have a historical past of submitting claims, even minor ones, this will point out a better future claims threat for the insurance coverage firm. This drives up house insurance coverage premiums.

- Homeowners’ credit score historical past: Just like with auto insurance coverage premiums, house insurers in some states use an individual’s credit-based insurance coverage rating to find out the chance that they might file a declare sooner or later.

- Homeowner’s marital standing: Married {couples} sometimes pay a decrease insurance coverage premium than their single counterparts as house insurers additionally understand them to be low threat.

Other components which will affect house insurance coverage charges embrace:

- Level of protection

- Deductible quantity

- Distance between the house and a fireplace hydrant or a fireplace station

- Distance from water

- Roof materials

- Pets

- Attractive nuisances, together with swimming pool, playground gear, and trampoline, which enhance legal responsibility potential

Life insurance coverage

All the variables that may have an effect on an individual’s life expectancy additionally have an effect on life insurance coverage premiums. These embrace:

- Age

- Gender

- Occupation

- Medical historical past

- Smoking standing

- Hobbies

Historically, charges are typically increased for males as a result of they usually have a shorter life expectancy than ladies. Certain professions – together with truck drivers, building employees, and legislation enforcement officers – additionally expose an individual to a increased threat of deadly accidents, pushing up premiums. The identical with involvement in excessive and journey sports activities.

Prices may additionally differ relying on the insurer and the kind of coverage. Permanent life insurance coverage insurance policies, for example, have increased premiums as a result of these present lifetime protection in comparison with time period life plans, which supply monetary safety solely inside a set time period.

Health insurance coverage

Health insurance coverage corporations can solely account for 5 components when figuring out premiums beneath the healthcare legislation, in keeping with the healthcare alternate web site Healthcare.gov. These are:

- Age: Premiums could be as much as thrice increased for older individuals than for youthful ones.

- Location: Differences in competitors, state, native rules, and value of residing additionally impression medical health insurance charges.

- Tobacco use: Insurers can cost tobacco customers as much as 50% greater than those that don’t smoke.

- Individual vs. household enrollment: Insurance suppliers may also cost extra for a plan that additionally covers a partner and dependents.

- Plan class: The totally different plan classes – Bronze, Silver, Gold, and Platinum – which point out how the prices are break up between the policyholder and the insurer, have an effect on insurance coverage premium costs.

The authorities web site additionally famous that states can restrict how a lot impression these components have on insurance coverage charges however prohibited them from utilizing medical historical past and gender in calculating premiums. You can try how medical health insurance plans work within the US and in numerous areas of the world in our well being protection information.

There generally is a large distinction between how a lot policyholders pay on premiums, relying on their private circumstances and a spread of insurance-related components. But there are additionally a number of sensible methods for them to avoid wasting on premium prices. Here are a few of them:

1. Comparing insurance coverage charges

Because every individual’s profile and circumstances are totally different, there is no such thing as a single coverage that’s the least expensive for everybody. An insurance coverage supplier that gives the most cost effective coverage for one individual is perhaps the costliest possibility for one more. The solely means for somebody to make sure they’re getting the bottom premiums doable is to match insurance coverage charges. This could be accomplished by means of varied insurance coverage comparability web sites which might be simply accessible on-line.

2. Taking benefit of reductions

Insurance suppliers provide a spread of reductions, which policyholders can reap the benefits of to scale back their annual premiums. These embrace:

- Bundling of auto insurance policies with owners’ or renters’ insurance coverage

- Insuring a number of autos in a single coverage

- Maintaining a clear driving file

- Paying premiums in full as a substitute of month-to-month instalments

- Installing safety and security options in properties and autos

- Being a member {of professional} organizations or affiliate teams

3. Skipping the pointless protection

Insurance corporations provide a spread of protection choices that impression how a lot premiums will price. Industry consultants recommend ditching the protection that policyholders won’t want to scale back charges. For those that are already lined by medical health insurance, for instance, they will take away or cut back medical funds protection from their auto insurance policy to chop prices.

4. Maintaining a great credit standing

In most states, insurers use an individual’s credit score rating in calculating automobile and residential insurance coverage premiums. This is completed as a result of there’s a correlation between an individual’s credit standing and the possibilities of submitting claims. Therefore, retaining one’s funds in verify might help policyholders save on insurance coverage prices.

5. Raising your deductible

A better deductible means policyholders can pay decrease premiums. But this additionally will increase the quantity they should pay earlier than their insurer picks up the tab within the occasion of an accident or loss. This is why it can be crucial for policyholders to be aware of the prices when taking this route to verify they’ve sufficient saved up in case of an emergency.

6. Shopping round when it’s time to resume

Unless they’re buying a time period life insurance coverage plan, which locks in a month-to-month charge for the total coverage time period, the premium quantity normally is just not set in stone. Most insurance policies final for six months or a yr, at which level the insurer will re-evaluate their threat degree which can impression insurance coverage charges. Because of this, consultants advise policyholders to overview their protection each time it renews and store round. A great way to seek out the most effective charges is to get at the very least three totally different quotes and go for the one that gives the most effective worth for his or her cash.

Premiums and deductibles are two of the most important out-of-pocket prices related to insurance coverage, which is why they might generally be confused with each other.

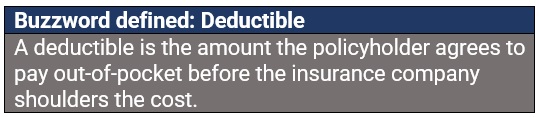

While an insurance coverage premium is the quantity a policyholder pays in alternate for protection, a deductible is the quantity the insured must pay for damages earlier than protection kicks in.

To illustrate, suppose a house owner has a $500 deductible for the dwelling protection on their house insurance coverage. If a storm causes $5,000 price of lined damages to their home, they might want to pay the $500 deductible for repairs whereas the insurance coverage firm covers the remaining $4,500.

One necessary factor to notice is that the upper the deductible, the decrease the insurance coverage premium, and vice versa. Because of this, selecting a better deductible could also be a great way to scale back insurance coverage prices, so long as the policyholder can afford to pay the out-of-pocket bills.

A single coverage may additionally have a number of deductibles as every protection might have its personal deductible quantity. The solely exception is medical health insurance, the place plan holders normally want to satisfy a single deductible for a whole calendar yr.

Almost all insurance coverage insurance policies include a deductible, apart from life insurance coverage, the place the beneficiaries obtain a tax-free lump-sum cost after the policyholder dies.

You can discover extra definitions of widespread insurance coverage business phrases in our jargon information.

Are there different features of insurance coverage premiums you need to focus on? Do you might have extra recommendations on how policyholders can save on insurance coverage prices? Chat us up on the feedback part beneath.

[ad_2]