{kind=link}

[ad_1]

Those with out company-sponsored medical health insurance, nevertheless, want to buy round for their very own plan and pay for the total price of protection. This begs the query – the place can they discover the perfect reasonably priced medical health insurance insurance policies?

In this text, Insurance Business discusses the completely different choices accessible for these trying to find reasonably priced medical health insurance. This is a part of our consumer schooling sequence and we encourage insurance coverage brokers and brokers to share this text with prospects to information them find the perfect well being plans that swimsuit their finances.

The newest evaluation by the nationwide well being non-profit Kaiser Family Foundation (KFF) pegged the typical month-to-month price of medical health insurance premiums at $456. The quantity an individual pays, nevertheless, may be decrease or considerably larger, relying on the place one lives.

New Hampshire residents, as an illustration, pay about $323 per individual month-to-month for medical health insurance – the most affordable primarily based on KFF’s newest benchmark premium. The quantity is greater than twice decrease than Vermont’s common at $841, which is the costliest month-to-month premium amongst all states.

But even when employer-sponsored protection shouldn’t be an possibility, there are a number of methods for a lot of Americans to avail of reasonably priced medical health insurance plans. Here are a few of them:

1. Medicaid

Considered essentially the most reasonably priced possibility, this government-funded well being program imposes sure eligibility standards, which fluctuate relying on the state they stay in. The legislation requires states to supply Medicaid help to those teams:

For those that fall into the above classes, they could avail of free or low-cost well being care in the event that they meet the next eligibility necessities.

- They are US residents or authorized aliens in good standing with immigration.

- They should be a resident of the state the place they’re making use of for protection.

- They should not presently be an inmate at an establishment, though they will apply for protection upon their launch.

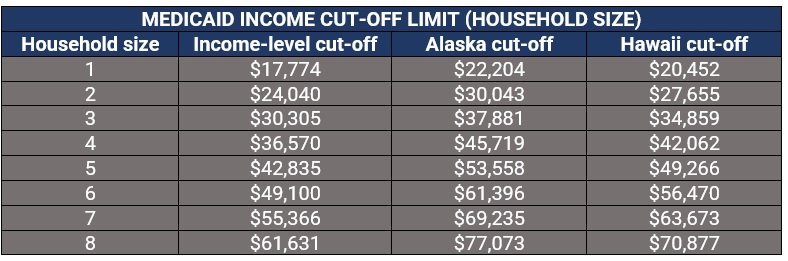

Currently, there are 38 states that enable earnings to be the only real foundation of qualification. The cut-off is often 133% of the federal poverty degree (FPL), which is about $17,774 per individual. An even bigger family means a better earnings restrict. The earnings cut-off is similar for nearly all 38 states, besides Alaska and Hawaii.

The desk beneath particulars the Medicaid cut-off restrict for every family measurement.

The remaining 12 states don’t provide income-only Medicaid qualification. These are:

- Alabama

- Florida

- Georgia

- Kansas

- Mississippi

- North Carolina

- South Carolina

- South Dakota

- Tennessee

- Texas

- Wisconsin

- Wyoming

In these states, the governments impose further eligibility standards, together with baby guardianship or being above 65-years previous.

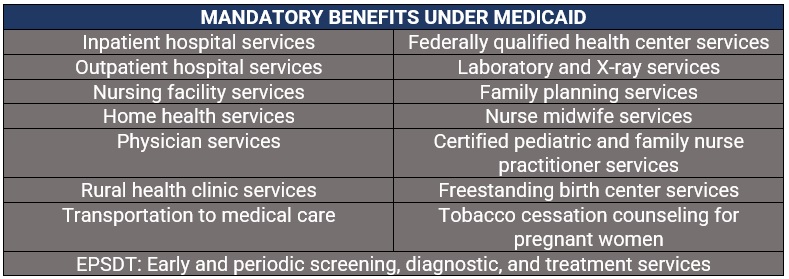

Medicaid plan holders have entry to free emergency care, household planning, and baby healthcare. Depending on their state and earnings ranges, they could even have copays for physician visits, inpatient hospital care, and prescription medicine.

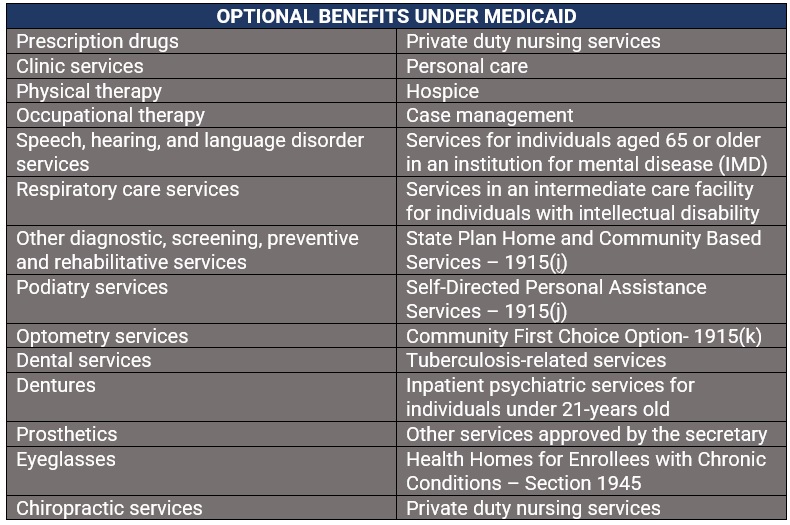

The tables beneath define the obligatory advantages that federal legislation requires every state to supply, together with the record of optionally available advantages.

2. Medicare

US residents and everlasting residents aged 65 and older can avail of reasonably priced medical health insurance by one other government-funded program, referred to as Medicare. The program can be accessible to youthful individuals with sure disabilities and people with end-stage renal illness (ESRD) or everlasting kidney failure that requires dialysis or a transplant.

Medicare consists of 4 elements:

- Medicare Part A (hospital insurance coverage): This covers inpatient hospital stays, care in a talented nursing facility, hospice care, and a few residence well being care.

- Medicare Part B (medical insurance coverage): This pays out for sure docs’ providers, outpatient care, medical provides, and preventive providers.

- Medicare Part C: Now referred to as the Medicare Advantage Plan, this combines all advantages and providers below Parts A and B in a single plan.

- Medicare Part D (prescription drug protection): This helps cowl the price of prescription medicine, together with most advisable pictures or vaccines.

The first two elements are supplied by the federal government, whereas the final two may be bought by non-public insurance coverage suppliers.

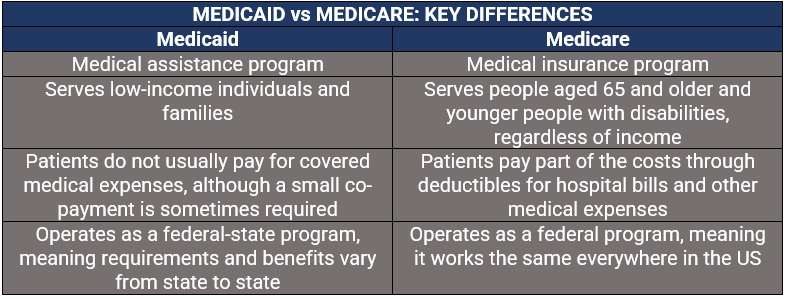

Because of their similar-sounding names, individuals are typically confused about what Medicaid and Medicare covers. Another issue that will add to the confusion is that in sure conditions, individuals might be able to apply for each.

To assist present some readability, Insurance Business summarized the important thing variations between these two government-administered applications within the desk beneath.

3. Health insurance coverage market

For many low-income Americans, their state’s medical health insurance market is one other good place to start out trying to find a coverage that matches their wants. Here, they will examine plans for protection and affordability, and get solutions to any questions or clarifications they could have about healthcare insurance coverage. This can be the place they will discover out in the event that they qualify for Medicaid, tax credit, or decrease premiums.

Parents can enroll their children within the Children’s Health Insurance Program (CHIP) by {the marketplace} as effectively. This program gives low-cost well being protection to kids in households whose earnings is simply too excessive to qualify for Medicaid, however not sufficient to afford non-public insurance coverage. In some states, CHIP additionally provides protection to pregnant ladies.

Individuals can join a medical health insurance plan throughout an open enrollment interval, which usually runs from November 1 by January 15. But even when this era has ended, they could nonetheless have the ability to safe protection if they’ve skilled a qualifying life occasion, together with getting married, having a child, and dropping their earlier insurance coverage. Coverage begins about two to 6 weeks after enrollment.

4. Short-term medical health insurance plans

Short-term medical health insurance plans are designed to fill non permanent protection gaps and supply safety for as much as one 12 months, so the advantages usually are not as complete as insurance policies within the market. Short-term plans may also be canceled anytime with out the necessity to pay penalty charges.

Because these usually are not regulated by the federal government, the advantages, protection limits, exclusions, and premiums fluctuate extensively, relying on the medical health insurance supplier. Coverage sometimes consists of doctor visits, and emergency and preventative care. Some plans might also cowl prescribed drugs. Pre-existing medical situations, nevertheless, usually are not lined.

Applicants might also be required to finish a medical questionnaire to help the insurance coverage provider in figuring out if they need to be accepted for reasonably priced medical health insurance protection.

5. Farm Bureau well being plans

Some states provide well being plans by the native Farm Bureau as an alternative choice to well being protection that complies with the Affordable Health Care Act (ACA). These states embrace:

- Tennessee

- Iowa

- Kansas

- Indiana

- South Dakota

The reasonably priced medical health insurance plans supplied by these native bureaus are typically inexpensive than ACA-compliant insurance policies. They are additionally exempted from state insurance coverage legal guidelines as states don’t think about Farm Bureau plans to be medical health insurance.

Enrollment is open year-round to Farm Bureau members. However, membership doesn’t require lively engagement within the agricultural sector and is as a substitute primarily based on the dues they pay. One essential factor to notice is that membership dues don’t cowl the price of the well being advantages, that are paid individually.

Farm Bureau well being plans additionally require medical underwriting, that means candidates may be rejected resulting from their medical historical past, in contrast to in ACA-compliant protection. They likewise impose ready durations for pre-existing situations.

Since these plans usually are not thought of medical health insurance, they don’t seem to be mandated to adjust to state or federal medical health insurance rules. This means protection doesn’t have to incorporate the ten important well being advantages below ACA and most out-of-pocket limits may be a lot larger.

According to HealthCare.gov, insurance coverage corporations can solely account for 5 elements when figuring out premiums below the healthcare legislation. These are:

- Age: Premiums may be as much as 3 times larger for older individuals than for youthful ones.

- Location: Differences in competitors, state, native rules, and value of dwelling additionally impression medical health insurance charges.

- Tobacco use: Insurers can cost tobacco customers as much as 50% greater than those that don’t smoke.

- Individual vs. household enrollment: Insurance suppliers may also cost extra for a plan that additionally covers a partner and dependents.

- Plan class: The completely different plan classes – Bronze, Silver, Gold, and Platinum – additionally impact premium costs.

The authorities web site famous that states can restrict how a lot impression these elements have on insurance coverage charges however prohibited them from utilizing medical historical past and gender in calculating premiums.

“Insurance companies can’t charge women and men different prices for the same plan,” HealthCare.gov defined. “They also can’t take your current health or medical history into account. All health plans must cover treatment for pre-existing conditions from the day coverage starts.”

Although the excessive price of well being plans can go away one feeling sick, there are a number of sensible steps that folks can take to save lots of on medical health insurance prices. Here are a few of them:

1. Consider your well being wants.

Because healthcare prices fluctuate relying on an individual’s particular person circumstances, it’s typically troublesome to find out which insurance policies provide the best financial savings – and typically premium costs usually are not the largest issue. Choosing a low premium, excessive deductible plan, as an illustration, can price the policyholder extra if they have an inclination to go to the physician extra typically. In such a state of affairs, it might be preferrred to pay larger premiums as this may additionally imply fewer out-of-pocket prices.

2. Avail of tax-advantaged plans.

Those in search of reasonably priced medical health insurance can avail of tax-advantaged plans that may assist them lower healthcare prices. These embrace:

- Health financial savings account (HSA): Available to policyholders with high-deductible well being plans (HDHPs), HSAs enable them to contribute funds to the account and withdraw them tax-free for certified medical prices, together with deductibles, copayments, and coinsurance.

- Health reimbursement association (HRA): As that is arrange and funded by employers, workers will be unable to contribute to the funds, however they will withdraw from their accounts for certified medical bills.

- Flexible spending account (FSA): Available from employers, FSAs enable employees to contribute pre-tax funds to the account and withdraw cash tax-free for certified medical prices.

HRAs and FSAs don’t require a high-deductible well being plan, however the funds should be utilized by the top of every 12 months. These accounts are additionally not moveable, that means if the worker leaves their firm, in addition they lose the account.

3. Get reasonably priced medical health insurance through the use of a premium tax credit score subsidy.

Those who’ve utilized by the medical health insurance market might have their charges diminished and even pay nothing for his or her plans in the event that they qualify for ACA’s premium tax subsidy. Plan holders whose family earnings is between 100% and 400% of the federal poverty degree (FDL) are eligible for subsidies on their well being insurance policies.

The subsidies work with {the marketplace} immediately sending the credit to the insurer who will then apply these to the plan’s month-to-month premiums to cut back the policyholder’s out-of-pocket bills. Plan holders should file a tax return on the finish of the 12 months to reconcile their earnings with the tax credit score they acquired. In some instances, they could need to pay again a number of the credit score that decreased their prices in the event that they earned extra earnings than anticipated after they first utilized for the well being plan.

4. Make certain you perceive your well being plans protection guidelines.

By doing so, policyholders can keep away from errors that can price them cash later. Some managed well being plans, for instance, cowl the prices if the plan holder chooses an in-network physician, however pay extra or the total price in the event that they go to an out-of-network medical skilled.

5. Review your medical health insurance plan yearly.

In preparation for open enrollment – the time of the 12 months after they can change company-sponsored or market well being protection – policyholders ought to reassess their well being must see if their present insurance policies nonetheless swimsuit them or in the event that they want further protection. By reviewing their insurance policies yearly, they are able to safe the perfect reasonably priced medical health insurance plan potential. Need assist? Check out the ten largest medical health insurance suppliers within the USA.

What about you? Do you have got any recommendations on get essentially the most reasonably priced medical health insurance plan potential that you just need to share? Hit us up within the feedback part beneath.

[ad_2]