{kind=link}

[ad_1]

We encourage insurance coverage brokers and brokers to share this text with their shoppers to assist them perceive this important type of protection.

In 2010, the US enacted the Affordable Care Act (ACA), a complete reform legislation aimed toward lowering healthcare prices for households and making certain that extra Americans have entry to medical health insurance. Under the ACA, sufferers who could also be uninsured due to restricted funds or pre-existing situations can now safe reasonably priced protection by means of their state’s medical health insurance market.

How does medical health insurance work within the US?

Through these medical health insurance marketplaces, Americans can select from a spread of coverages designed to satisfy completely different healthcare wants.

“Some types of plans restrict your provider choices or encourage you to get care from the plan’s network of doctors, hospitals, pharmacies, and other medical service providers,” in accordance with the federal government’s medical health insurance alternate web site HealthCare.gov. “Others pay a greater share of costs for providers outside the plan’s network.”

Here are some varieties of plans that individuals can entry by means of these medical health insurance marketplaces:

Health Maintenance Organization (HMO)

This sort of medical health insurance plan usually limits protection to care from docs who work for or are contracted with the HMO. Policies typically don’t cowl out-of-network care besides in an emergency. Plans could likewise require {that a} policyholder reside or work in its service space to be eligible for protection. HMOs usually present built-in care and give attention to prevention and wellness.

Exclusive Provider Organization (EPO)

This is a managed care plan the place companies are lined provided that the docs, specialists, or hospitals are within the plan’s community – besides in circumstances of emergency. This signifies that if a policyholder opts for an out-of-network supplier, they must cowl the complete value of therapy themselves.

Point of Service (POS)

In this sort of plan, policyholders pay much less in the event that they entry docs, hospitals, and different healthcare suppliers belonging to the plan’s community. POS protection additionally requires the insured to get a referral from their major care physician for them to see a specialist.

Preferred Provider Organization (PPO)

This well being plan permits policyholders to pay much less for healthcare in the event that they select to get therapy from suppliers within the plan’s community. However, they will additionally entry docs, hospitals, and suppliers outdoors of the community with no referral for a further value.

HealthCare.gov added that US medical health insurance plans are provided in 4 classes based mostly on how the prices are break up between the policyholder and the insurer. Also known as the “metal tiers,” these plans are:

- Bronze: 60% well being insurer, 40% policyholder

- Silver: 70% well being insurer, 30% policyholder

- Gold: 80% well being insurer, 20% policyholder

- Platinum: 90% well being insurer, 10% policyholder

What does medical health insurance within the US cowl?

One of the adjustments the ACA has carried out is the standardization of insurance coverage plan advantages within the nation’s healthcare system. Before this, the advantages provided different considerably relying on the insurance coverage firm and the kind of coverage. At current, US medical health insurance plans are required to cowl these 10 “essential health benefits.”:

- Ambulatory affected person companies

- Emergency companies

- Hospitalization

- Laboratory companies

- Mental well being and substance use dysfunction companies, together with behavioral well being therapy

- Pediatric companies, together with oral and imaginative and prescient care

- Pregnancy, maternity, and new child care

- Prescription medicine

- Preventive and wellness companies and continual illness administration

- Rehabilitative and habilitative companies and gadgets

Birth management and breastfeeding protection are additionally required advantages. Dental and eye care protection for adults, in the meantime, aren’t thought of important advantages however can be found as non-obligatory add-ons, together with medical administration applications.

How a lot does medical health insurance value within the US?

Health insurance coverage premiums throughout the US value a mean of $456 month-to-month per particular person, in accordance with the most recent market benchmark premiums from the Kaiser Family Foundation. This could be a steep value to pay for some American households.

For many employed people, this might not be a trigger for concern as their employers cowl about four-fifths of their medical health insurance prices. But these with out entry to company-sponsored protection want to buy round for their very own well being plan and canopy the complete value of premiums.

According to HealthCare.gov, well being insurers can solely account for 5 components when figuring out premiums beneath the ACA. These are:

- Age: Premiums may be as much as thrice increased for older Americans than for his or her youthful counterparts.

- Location: Differences in competitors, state, native laws, and value of residing additionally dictate medical health insurance charges.

- Tobacco use: Insurers can cost tobacco customers as much as 50% greater than those that aren’t into smoking.

- Individual vs. household enrollment: Insurance suppliers can cost extra for a plan that additionally covers a partner and dependents.

- Plan class: The completely different steel tiers – Bronze, Silver, Gold, and Platinum – additionally impression premium costs.

States can restrict how a lot these components have an effect on insurance coverage charges however are prohibited from utilizing medical historical past and gender in calculating premiums.

“Insurance companies can’t charge women and men different prices for the same plan,” HealthCare.gov defined. “They also can’t take your current health or medical history into account. All health plans must cover treatment for pre-existing conditions from the day coverage starts.”

Health insurance coverage suppliers within the US provide fundamental insurance policies to people and companies – together with different companies that may embody Medicaid and Medicare insurance policies, long-term care insurance coverage, dental protection, and imaginative and prescient advantages. The prime 10 medical health insurance corporations within the nation management nearly two-thirds of the market.

Canada’s healthcare system is thought to be top-of-the-line on this planet, offering all residents and everlasting residents free entry to emergency care and common physician visits. However, there are nonetheless sure companies that Medicare – the nation’s common well being protection – doesn’t cowl, which Canadians have to pay for.

How does Canada’s healthcare system work?

Canada has a publicly funded healthcare system that operates beneath the Canada Health Act (CHA). To be eligible to obtain full federal money contributions, every provincial and territorial medical health insurance plan must adjust to the 5 pillars of the CHA, which stipulates the that insurance policies have to be:

- Universal

- Publicly administered

- Comprehensive protection situations

- Portable throughout provinces and territories

- Accessible (as an illustration, with out person charges)

“Health care is funded and administered primarily by the country’s 13 provinces and territories,” in accordance with the Commonwealth Fund, a personal non-profit group that helps unbiased analysis on well being care points and supplies grants aimed toward bettering the nation’s well being system. “Each has its own insurance plan, and each receives cash assistance from the federal government on a per-capita basis.”

The group added that whereas advantages and supply approaches range, all Canadian residents and everlasting residents obtain “medically necessary hospital and physician services free at the point of use.”

However, not every part is roofed by Medicare. These embody:

- Eye and dental care

- Outpatient prescribed drugs

- Rehabilitation companies

- Private hospital rooms, which Canadians have to pay for out of pocket.

Canadians have to pay out of pocket for these, so it isn’t shocking that, though not required, almost 70% of Canadians have taken out supplemental non-public well being protection, in accordance with the most recent figures from the Canadian Life and Health Insurance Association (CLHIA). Of these, 90% have been bought by means of group plans.

What does Canada’s common healthcare system cowl?

Canadian Medicare covers lots of the healthcare fundamentals, together with:

- Doctor and hospital visits

- Diagnostics and examinations

- Eye examinations for Canadians aged beneath 18 or over 65

- Medically vital dental surgical procedures

- Standard lodging within the hospital (together with care, meals, and prescriptions)

- Surgeries and coverings

Each province and territory implement their very own guidelines in terms of well being protection, so the exclusions could range. For the next objects and companies, non-public medical health insurance could also be vital for protection, relying on the place an individual lives.

- Ambulance and EMT companies

- Dental care

- Massage remedy

- Medical tools (together with wheelchairs, crutches, and leg braces)

- Outpatient prescription drugs

- Physiotherapy

- Prescription eyeglasses

- Private hospital room stays

- Psychological companies

How a lot does non-public medical health insurance value in Canada?

The newest out there figures from the Canadian Institute for Health Information (CIHI) estimated the price of non-public medical health insurance at $756 per 12 months, which is equal to $63 month-to-month. The institute’s information additionally confirmed that the typical Canadian paid out $902 in out-of-pocket well being bills, or barely over $75 every month.

These numbers, nevertheless, have been taken earlier than COVID-19 shook not simply Canada’s healthcare system but in addition that of the world, so the values would possibly truly be increased at current. In addition, the figures above are mere estimates and the easiest way to get an correct quantity is to contact the medical health insurance corporations instantly.

Canada is dwelling to about 130 non-public medical health insurance suppliers, serving a complete of 27 million Canadians. These corporations provide among the greatest supplemental well being protection.

The UK has a publicly funded healthcare system, known as the National Health Service (NHS), which everybody residing within the nation can entry without spending a dime.

The NHS operates a residence-based mannequin somewhat than an insurance-based system. This signifies that anybody residing and dealing within the UK, even these on a short lived work visa, is entitled to free healthcare by means of the NHS.

The NHS presents a big selection of companies, from major care to specialised remedies. These embody:

- Consultations with a basic practitioner (GP) or nurse

- Contraception and sexual well being companies

- Maternity companies

- Hospital therapy in accidents and emergencies (A&E)

- Treatment of minor accidents in clinics

- Treatment with a specialist or guide if referred by a GP

But similar to the general public healthcare methods in different nations, the quantity of individuals accessing the NHS has resulted in lengthy ready occasions. Because of this, UK residents can choose to take out non-public medical health insurance, which permits them to entry specialists extra shortly and use higher services.

How does non-public medical health insurance work within the UK?

Private well being insurance policies within the UK are designed to cowl the price of non-public therapy for acute situations. This means most well being plans present protection for short-term, curable medical points, somewhat than continual sicknesses, which individuals are inclined to reside with all through their lifetimes.

There are a number of varieties of non-public medical health insurance that Brits can entry. These embody:

- Individual medical health insurance: Provides entry to non-public medical care for many who aren’t insured by their employers.

- Family medical health insurance: Allows the policyholder and their family members to entry non-public medical care.

- Health insurance coverage for youngsters: Provides non-public medical care for youngsters 18-years previous and youthful, though the age requirement may be prolonged for these in full-time training.

- Company medical health insurance: Gives workers entry to non-public medical care.

- Health insurance coverage for over 50s: Allows individuals aged 50 and older to entry non-public medical companies.

What are the professionals and cons of personal medical health insurance within the UK?

Taking out non-public medical health insurance yields the next advantages:

- Faster entry to well being care on the level of want

- Control over the place and when to get therapy and who conducts the therapy

- Access to a personal room as a substitute of being confined to a busy ward

- Option to obtain specialist medicine and therapy unavailable on the NHS

However, there are additionally drawbacks and drawbacks of personal medical health insurance:

- The excessive value of protection

- Some remedies and companies are excluded

- Usually comes with an extra

- Most remedies lined may be accessed without spending a dime with the NHS

- Private hospitals usually should not have an A&E division

How a lot does non-public medical health insurance value within the UK?

An evaluation performed by London-based private finance web site NimbleFins has discovered that the typical value of personal medical health insurance within the UK is round £85 a month or £1,200 yearly.

Just like in different areas, premium costs are impacted by a spread of things. These embody the policyholder’s:

- Age

- Residence

- Smoking standing

- Previous well being situations

- Claims historical past

Despite gaining access to top-of-the-line public healthcare methods on this planet, Australians should still have to endure lengthy ready occasions for non-life-threatening procedures. And similar to in Canada, they could additionally have to pay for sure companies that the nation’s common medical health insurance, additionally known as Medicare, doesn’t cowl.

This is the rationale why the Australian authorities is encouraging residents to take out non-public medical health insurance by means of tax incentives and premium rebates.

How does non-public medical health insurance work in Australia?

Private medical health insurance in Australia pays out for medical bills which might be not lined beneath the general public healthcare system. It can even cowl the price of therapy in a personal hospital or if one chooses to be handled as a personal affected person in a public hospital. Australians should buy insurance policies solely from registered well being insurers.

There are two predominant varieties of non-public well being protection:

- Hospital cowl: Pays out the price of therapy in a public or non-public hospital.

- Extras cowl: Also known as basic therapy cowl, this pays for the prices of medical companies that Medicare doesn’t cowl.

Citizens and everlasting residents in most states and territories can even safe ambulance cowl, which incorporates emergency transport and medical care. The exceptions are Queensland and Tasmania, the place the state governments present automated protection for residents.

What are the advantages of taking out non-public medical health insurance in Australia?

The nation’s Department of Health listed 4 predominant benefits of taking out this sort of protection on its official web site. These are:

- More well being cowl and choices: Private medical health insurance offers policyholders the choice to get therapy in a personal hospital the place ready occasions for non-urgent procedures are a lot shorter. They can even select to be handled by their most well-liked physician.

- Tax incentives: Policyholders can keep away from paying the Medicare Levy Surcharge (MLS), a sort of tax imposed on Australians who should not have non-public hospital cowl and earn a sure stage of earnings. This levy is aimed toward encouraging individuals to take up non-public insurance coverage to scale back the stress on the general public well being system.

- Premium rebates: Most Australians who’ve taken out non-public well being protection obtain an “income-tested” rebate from the federal government to assist cowl the price of their premiums.

- Avoid paying LHC loading: Australians who purchased non-public hospital cowl earlier than turning 31 beginning on 1 July 2000 – additionally known as their “lifetime health cover base day” – and have maintained protection since can keep away from paying an additional quantity known as “lifetime health cover loading.” Those who didn’t could pay increased premiums for personal hospital cowl for the subsequent 10 years.

How a lot does non-public medical health insurance value in Australia?

Premium costs of personal well being cowl in Australia are influenced by a number of components. These embody the quilt sort and tier, how many individuals a coverage covers, and the policyholder’s age, earnings, and residence.

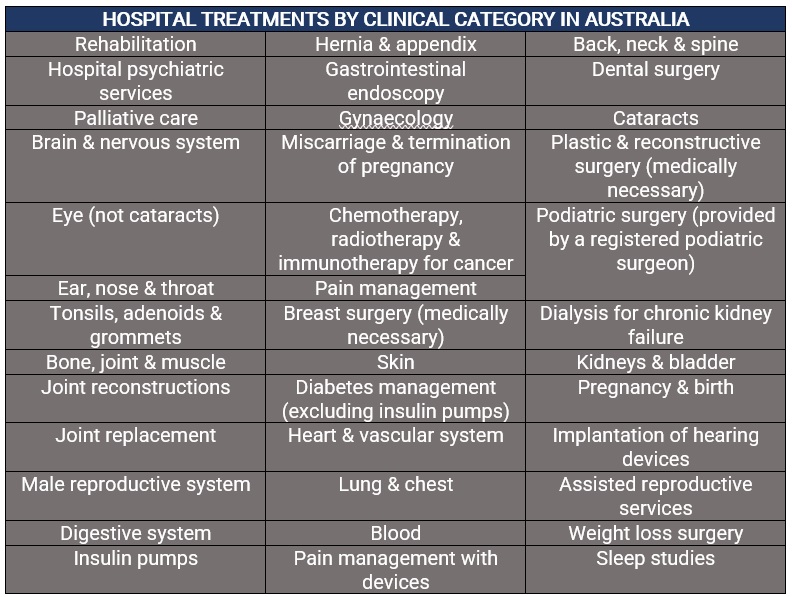

Hospital cowl is on the market in 4 completely different tiers, specifically Gold, Silver, Bronze, and Basic, every masking a mandated checklist of remedies. Because Gold insurance policies cowl all 38 varieties of remedies outlined by the federal government, additionally they include the most costly premiums.

An evaluation by the comparability web site Finder pegged the price of a hospital cowl for a gold coverage at about $228 a month. Monthly premiums for fundamental, bronze, and silver insurance policies are estimated to be $99, $120, and $180, respectively. For additional cowl, the typical is $68 per single coverage per thirty days.

Every 12 months, the Private Health Insurance Ombudsman (PHIO) releases a State of the Health Funds report to supply each customers and trade specialists with comparative data on the efficiency and repair supply of all well being insurers throughout the nation. The report additionally ranks the prime non-public medical health insurance suppliers in Australia based mostly on a set of key indicators.

Is non-public medical health insurance one thing you’re contemplating taking out? Is there something you wish to add that we’d have missed? Share your ideas in our feedback part under.

[ad_2]