{kind=link}

[ad_1]

We encourage insurance coverage brokers and brokers to share this text with their purchasers to assist them determine which enterprise insurance coverage insurance policies are important to maintain them protected.

One of the largest benefits of taking out insurance coverage for companies is the monetary safety it offers when sudden losses happen. As they carve out the trail to success, firms might face conditions that may adversely affect their profitability. Mistakes can result in expensive lawsuits, whereas accidents and calamities can take an enormous chunk out of their income. Having the appropriate insurance policies performs an important position in serving to their enterprise get well sooner.

Carrying enterprise insurance coverage additionally boosts an organization’s credibility as many stakeholders and purchasers want working with companies that they know are financially protected.

Taking out enterprise insurance coverage, nevertheless, is only one aspect of how firms can reduce their losses. Pairing insurance coverage protection with good danger administration practices is usually the easiest way companies can defend their property and funds.

Because every enterprise faces their very own share of distinctive dangers and challenges, there isn’t any one-size-fits-all coverage that covers each want. The kind of insurance coverage that firms would require relies on a number of elements, together with their enterprise actions, dimension, and site.

Business insurance coverage suppliers supply a variety of insurance policies that may assist defend firms in opposition to the completely different dangers they face. The choice is various, however in line with trade insiders, these are a few of the most important coverages that companies want to take care of their operations when accidents and disasters strike.

1. General legal responsibility insurance coverage

General legal responsibility insurance coverage, additionally referred to as enterprise legal responsibility or public legal responsibility protection, protects firms in opposition to claims of bodily damage or property harm ensuing from their enterprise actions. This kind of coverage may present protection for reputational hurt and copyright infringement.

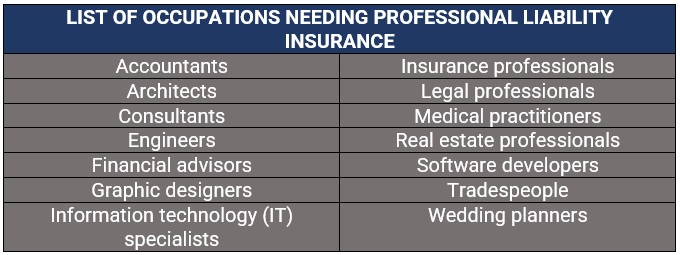

2. Professional legal responsibility insurance coverage

Also often called errors and omissions (E&O) or malpractice insurance coverage, this type of protection protects the enterprise from work-related claims, together with mismanagement, sexual harassment, and discrimination. It covers authorized and settlement prices arising from service-related errors and oversights, breach of contract, unfinished work, and price range overruns, amongst others.

Professional legal responsibility insurance coverage not solely covers administrators and govt administration but in addition different workers and the enterprise itself. Although not at all times legally required, having this type of protection is important for a lot of firms, particularly for people who present skilled or advisory providers.

3. Product legal responsibility insurance coverage

For companies that promote merchandise, product legal responsibility protection could also be price contemplating. This protects the corporate in opposition to lawsuits from clients claiming losses or damage due to their product. This kind of economic insurance coverage coverage additionally covers authorized protection prices and compensation if the enterprise is discovered to be at fault.

4. Directors’ and officers’ (D&O) insurance coverage

D&O insurance coverage, additionally known as D&O legal responsibility insurance coverage, is designed to defend the administrators and senior administration of an organization in opposition to monetary losses ensuing from business-related lawsuits. This kind of coverage pays out for financial losses from these authorized actions, together with protection prices, settlements, and fines.

D&O protection is available in three principal sorts, additionally known as insuring agreements or sides, with every providing completely different ranges of safety:

- Side A: Covers “non-indemnifiable loss” or conditions the place the enterprise can not indemnify its administrators or officers, both on account of chapter or as a result of they aren’t legally allowed to take action.

- Side B: The mostly accessed insuring settlement, this works by reimbursing an organization after it has compensated a director or different senior administration for a loss, together with protection prices, settlements, and judgments.

- Side C: Also referred to as entity protection, this offers direct protection for a enterprise when each the corporate and its administrators and senior administration are named in a lawsuit.

5. Commercial property insurance coverage

Commercial property insurance coverage, additionally known as enterprise property or business constructing insurance coverage, is designed to attenuate disruption to an organization’s day-to-day operations by providing compensation for damages or losses that occur to the next:

- Property or constructing the enterprise operates in

- Equipment and know-how the corporate makes use of

- Inventory of merchandise and supplies the enterprise shops and sells

Some insurance policies additionally pay out a portion of misplaced revenue if the harm prevents a enterprise from conducting its standard operations. Business property protection is usually a requirement for business leasing preparations.

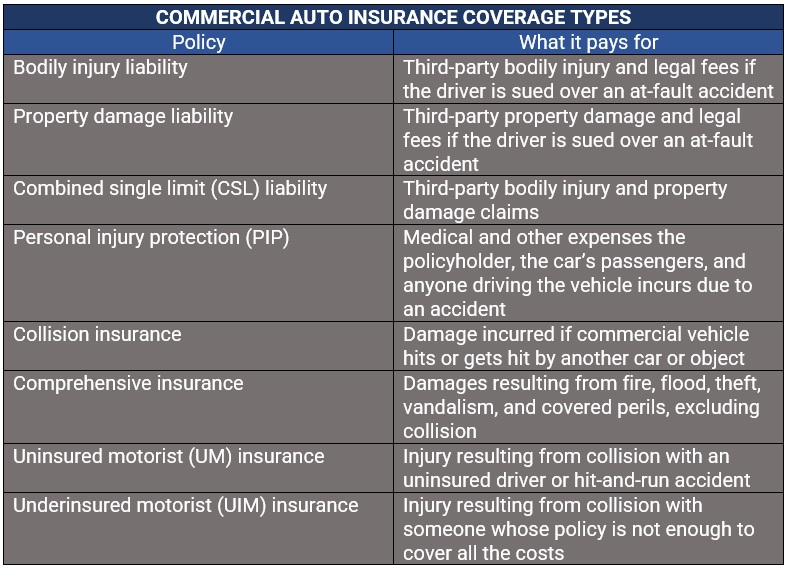

6. Commercial auto insurance coverage

Commercial auto insurance coverage is a sort of automotive coverage designed for automobiles pushed for enterprise functions. In phrases of safety, it really works equally to non-public auto insurance coverage however covers primarily firm vehicles and business vehicles and vans.

7. Health insurance coverage

Businesses that make use of greater than 50 full-time workers are required to take out medical health insurance for his or her staff, in line with the Affordable Care Act (ACA). For these with lower than 50 staff, the ACA gives a Small Business Health Options Program (SHOP) as protection.

8. Workers’ compensation insurance coverage

Workers’ compensation insurance coverage, additionally referred to as staff’ comp protection, pays out the price of medical care and a part of the misplaced revenue of staff who get sick or injured whereas performing their jobs. It additionally protects the companies from the monetary legal responsibility of getting to pay for bills arising from work-related sicknesses and accidents out of pocket.

Workers’ compensation insurance coverage insurance policies present a number of sorts of coverages, together with:

- Medical bills: Covers the price of medical therapy for the sick or injured employee.

- Lost revenue: Pays out a part of the worker’s wage if they should take day off from work due to the sickness or damage they sustained.

- Ongoing care: Covers bills incurred if the worker requires prolonged medical care on account of a work-related damage or sickness, together with rehabilitation prices.

- Disability advantages: Covers medical payments and a few misplaced wages of staff who change into disabled due to a office accident.

- Death advantages: Pays out funeral and burial bills and offers monetary advantages for beneficiaries of staff who die on account of a job-related damage or sickness.

9. Business interruption insurance coverage

Business interruption insurance coverage, additionally referred to as BI or enterprise revenue protection, is designed to guard firms in opposition to monetary losses incurred from the disruption of their operations ensuing from an insured peril. We will focus on this kind of coverage intimately in our protection highlighted under.

10. Cyber insurance coverage

Cyber insurance coverage are designed to guard companies in opposition to monetary losses ensuing from cyber incidents. Policies sometimes present two sorts of safety:

First-party protection

This kind of protection pays out for the monetary losses the enterprise incurs on account of a cyber incident, together with:

- Cost of responding to a knowledge breach

- Cost of restoring and recovering misplaced or broken knowledge

- Lost revenue ensuing from enterprise interruption

- Ransomware assault funds

- Risk evaluation of future cyberattacks

- Cost of informing clients concerning the cyber incident

- Anti-fraud providers

Third-party protection

This offers monetary safety in opposition to lawsuits filed by third events, together with clients, staff, and distributors, for damages brought on by a cyberattack on the enterprise. Policies sometimes cowl courtroom and settlement charges, and regulatory fines.

Every 12 months, insurance coverage behemoth Allianz surveys hundreds of companies from about 90 international locations and territories and greater than 20 industries to search out out which dangers these firms see as posing the best menace to their operations. Here are the ten largest dangers companies throughout the globe are going through, in line with Allianz’s newest Risk Barometer report.

- Cyber incidents – corresponding to cyberattacks, IT failure or outage, knowledge breaches, and their corresponding fines and penalties.

- Business interruption – together with provide chain disruption

- Natural catastrophes – together with storms, flooding, earthquakes, wildfire, and different climate occasions

- COVID-19 outbreak – corresponding to well being and workforce points, and restrictions on motion

- Changes in laws and regulation – together with commerce wars and tariffs, financial sanctions, protectionism, Brexit, and Euro-zone disintegration

- Climate change – corresponding to bodily, operational, monetary, and reputational dangers ensuing from world warming

- Fire and explosion

- Market developments – corresponding to volatility, intensified competitors and new entrants, M&A, market stagnation, and market fluctuation

- Shortage of expert workforce

- Macroeconomic developments – together with financial insurance policies, austerity packages, commodity worth will increase, deflation, and inflation

The disruption led to by the COVID-19 pandemic has given prominence to this kind of protection, which has additionally been the purpose of competition between insurers and their policyholders. In essence, enterprise interruption or BI cowl is designed to guard companies from lack of revenue and extra prices incurred if their operations are pressured to close down due to an sudden occasion. Insurance firms, nevertheless, argue that the loss ought to end result from “material damage caused to property.”

How does enterprise interruption insurance coverage work?

Business interruption insurance coverage offers firms monetary safety for the losses they endure due to the disruption to their operations brought on by an insured occasion. It pays out the working prices whereas the enterprise briefly shuts down. These prices embrace:

- Potential income

- Mortgage or lease on business area

- Business mortgage repayments

- Employee salaries

- Taxes

Some insurance policies additionally present protection for added bills associated to the closure corresponding to these accompanying the organising of a short lived location or the coaching of workers to make use of new gear.

For small and medium-sized enterprises, BI protection is usually included in a enterprise proprietor’s coverage, which bundles completely different coverages firms want, together with normal legal responsibility, business property, and staff’ compensation cowl.

Business interruption insurance policies sometimes entail a 48- to 72-hour ready interval to kick in. This is indicated within the coverage’s restoration interval, which initially lasts for 30 days however might be prolonged to as much as a 12 months.

What are the highest causes of enterprise interruption?

A five-year knowledge evaluation of insurance coverage claims carried out by main insurer AGCS has discovered that fireside and explosion have been the main causes of enterprise disruption globally, accounting for 30%, or $6.7 million price, of all BI losses. This was adopted by storms (21%), water harm (12%), equipment breakdown (5%), and flooding (4%).

In phrases of enterprise interruption triggers, 52% of respondents mentioned cybercrime, which was pushed by the current spate of ransomware assaults, was the one they feared probably the most, adopted by pure catastrophes (36%), pandemic outbreaks (35%), and transportation and transport disruptions (30%).

Does enterprise interruption insurance coverage cowl COVID-19-related losses?

Whether enterprise interruption insurance policies ought to cowl losses brought on by the coronavirus pandemic has been a contentious challenge between insurance coverage firms and companies affected by the outbreak. The insurance coverage trade has maintained that pandemics can’t be coated due to the dimensions of their affect.

“Pandemics are an extraordinary catastrophe that can impact nearly every economy in the world, so it is hard to predict and manage the risk,” mentioned Sean Kevelighan, chief govt officer on the Insurance Information Institute (Triple-I), in a 2020 assertion. “Pandemic-caused losses are excluded from standard business interruption policies because they impact all businesses, all at the same time.”

This, nevertheless, has not prevented firms looking for compensation from taking their arguments to courtroom. The University of Pennsylvania Carey Law School’s COVID-19 protection litigation tracker has recorded greater than 2,300 lawsuits over enterprise revenue protection, with nearly all of lawsuits coming from firms within the meals providers sector.

Early final 12 months, the UK Supreme Court dismissed appeals by insurance coverage firms in a check case introduced by the Financial Conduct Authority (FCA) on behalf of policyholders. The insurers argued that many BI insurance policies didn’t cowl widespread disruption ensuing from the restrictions imposed by the federal government to curb the unfold of the coronavirus in 2020. After scrutinizing non-damage insurance coverage coverage clauses, which cowl illness, denial-of-access-to-business-premises, and hybrid clauses, the Supreme Court unanimously dismissed the appeals, a ruling that has large implications for the insurance coverage trade worldwide.

What do firms want to contemplate when taking out enterprise insurance coverage?

There are a number of elements that firms want to contemplate earlier than taking out enterprise insurance coverage. These embrace:

- The firm’s enterprise construction

- The trade the place the enterprise operates

- The sorts of dangers the corporate faces

- The firm’s dimension or variety of staff

- Whether the corporate has enterprise premises or automobiles

- The inventory, gear, and instruments the corporate owns

It would even be useful for companies to seek the advice of an skilled insurance coverage agent or dealer who may give them sound recommendation concerning which coverages swimsuit their operations the most effective.

Do you need assistance discovering the appropriate protection for what you are promoting? What sorts of insurance policies do you suppose are important? Use the feedback field under to share your ideas.

[ad_2]