{kind=link}

[ad_1]

In this text, Insurance Business lists down the completely different insurance coverage sorts everybody ought to think about buying to make sure they’re financially protected. This is a part of our consumer training collection, and we encourage insurance coverage brokers and brokers to share this text with prospects to assist them type by the completely different coverages accessible.

Here are the primary insurance coverage sorts that many trade specialists say are price taking out and the way every protection kind works in numerous elements of the world.

In most areas, motorists are required to hold no less than a sure stage of protection to legally function a car. Getting caught driving with out one may end up in hefty penalties and should influence future eligibility for acquiring protection.

United States

In the US, practically each state mandates that drivers need to have the following coverages, in accordance with the Insurance Information Institute (Triple-I):

- Bodily harm legal responsibility: Covers medical and authorized prices related to accidents or dying for which the driving force is at-fault.

- Property injury legal responsibility: Pays out if the policyholder’s car damages one other individual’s property, in addition to authorized prices incurred in a lawsuit.

- Medical funds (Med Pay) or private harm safety (PIP): Covers medical bills for accidents the policyholder and their passengers maintain in an accident. Some insurance policies additionally pay out for misplaced earnings.

- Uninsured/underinsured motorist protection (UM/UIM): Pays out for accidents the policyholder and their passengers undergo if they’re hit by an uninsured or underinsured driver.

Canada

Canadian provinces and territories have their very own guidelines and laws in the case of necessary protection. Because every implement different automotive insurance coverage methods, there are additionally various necessities. But there are additionally similarities. These are:

- Third-party legal responsibility: Covers the price of lawsuits if the policyholder is chargeable for an accident that causes bodily harm, dying, or property injury.

- Uninsured vehicle/motorist: Provides protection if the policyholder or their passenger is injured or killed by an uninsured driver or in a hit-and-run incident. But in contrast to within the US, this additionally covers damages to the policyholder’s car.

- Accident advantages: Pays out for medical therapies and earnings alternative if the policyholder is injured in an accident and funeral bills ought to they succumb to their accidents, no matter who’s at-fault. This works just like Med Pay or PIP within the US.

United Kingdom

In the UK, the federal government requires drivers to take out third-party insurance coverage. This covers injury or harm attributable to the policyholder to a different individual, car, animal, or property. Just like legal responsibility protection in different international locations, it doesn’t cowl damages to the policyholder’s car.

Australia

Australia mandates that drivers carry no less than one kind of protection – obligatory third-party (CTP) insurance coverage. Also referred to as inexperienced slip insurance coverage in New South Wales or transport accident cost (TAC) in Victoria, CTP insurance coverage covers the driving force’s legal responsibility if different persons are injured or killed in a vehicular accident. This kind of coverage, nonetheless, doesn’t cowl accidents to the driving force and their passengers, and damages to any car or property. This kind of protection is paid for when automotive homeowners renew their car registration.

Health insurance coverage insurance policies are aimed toward serving to policyholders offset the prices of medical therapy by overlaying part of the skilled and hospital charges the policyholder incurs. Because every nation implements a special public healthcare system, the extent of want for personal well being plans additionally varies.

United States

Due to the excessive price of healthcare within the US, taking out medical health insurance is important for a lot of Americans to have the ability to afford the mandatory medical care. According to the federal government’s medical health insurance alternate web site HealthCare.gov, well being protection is available in a number of varieties aimed toward assembly the various wants of policyholders.

Among the sorts of insurance policies at present accessible available in the market are:

- Exclusive Provider Organization (EPO): A managed care plan the place providers are coated provided that the docs, specialists, or hospitals are within the plan’s community, besides in emergency instances.

- Health Maintenance Organization (HMO): Limits protection to care from docs who work for or are contracted with the HMO.

- Point of Service (POS): Policyholders pay much less in the event that they entry docs, hospitals, and different healthcare suppliers belonging to the plan’s community.

- Preferred Provider Organization (PPO): Lets policyholders pay much less for healthcare in the event that they select to get therapy from suppliers within the plan’s community, though they will additionally entry docs, hospitals, and suppliers outdoors of the community with out a referral for an extra price.

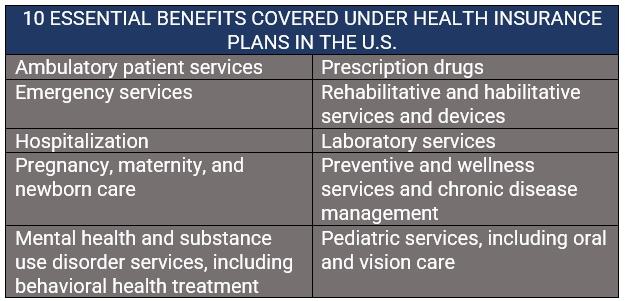

US medical health insurance plans are required to cowl an inventory of 10 “essential health benefits.” This is the results of the standardization of insurance coverage plan advantages beneath the Affordable Healthcare (ACA).

Birth management and breastfeeding protection are additionally required advantages. Dental and eye care coverages for adults and medical administration applications, nonetheless, usually are not thought of important advantages, however can be found as non-obligatory extras.

Canada

Canada’s healthcare system is thought to be among the best on this planet, offering all residents and everlasting residents free entry to emergency care and common physician visits. However, there are nonetheless sure providers that Medicare – the nation’s common well being protection – doesn’t cowl. These embody eye and dental care, outpatient prescribed drugs, rehabilitation providers, and personal hospital rooms, which Canadians have to pay for, both out of pocket or by supplemental personal insurance coverage.

The nation’s public healthcare system covers lots of the “basics.” These embody:

- Doctor and hospital visits

- Diagnostics and examinations

- Eye examinations for Canadians aged beneath 18 or over 65

- Medically vital dental surgical procedures

- Standard lodging within the hospital, together with care, meals, and prescriptions

- Surgeries and coverings

Each province and territory implement their very own guidelines in the case of well being protection, so the exclusions could fluctuate. For the next objects and providers, personal medical health insurance could also be vital to acquire cowl, relying on the place an individual resides.

- Ambulance and EMT providers

- Dental care

- Massage remedy

- Medical tools, together with wheelchairs, crutches, and leg braces

- Outpatient prescription medicines

- Physiotherapy

- Prescription eyeglasses

- Private hospital room stays

- Psychological providers

United Kingdom

UK residents and everlasting residents are entitled to free healthcare by the National Health Service (NHS). Coverage usually consists of:

- Consultations with common practitioner (GP) or nurse

- Hospital therapy in accidents and emergencies (A&E)

- Treatment of minor accidents in clinics

- Treatment with a specialist or advisor if referred by a GP

- Contraception and sexual well being providers

- Maternity providers

People even have the choice to take out personal medical health insurance, which permits them to entry specialists extra shortly, keep away from lengthy ready occasions, and use higher amenities.

Australia

Despite accessing among the best public healthcare methods on this planet, Australians should still have to endure lengthy ready occasions for non-life-threatening procedures. They can also have to pay for sure providers that Medicare – the nation’s common medical health insurance – doesn’t cowl. These embody ambulance, dental, optical, and chiropractic care.

This is the explanation why the federal government is encouraging residents to take out personal medical health insurance by tax incentives and premium rebates.

Private medical health insurance in Australia is designed to pay out for medical bills that aren’t coated beneath the general public healthcare system and Medicare. It also can cowl the price of therapy in a non-public hospital or if one chooses to be handled as a non-public affected person in a public hospital. Policies should be purchased from registered well being insurers.

Private well being protection is available in two most important sorts:

- Hospital cowl: Pays out the price of therapy in a public or personal hospital.

- Extras cowl: Also known as common therapy cowl, pays out the prices of medical providers that Medicare doesn’t cowl.

Ambulance cowl, which incorporates emergency transport and medical care, may also be bought in most states and territories, besides in Queensland and Tasmania as these states already present automated protection for everlasting residents.

Life insurance coverage works virtually precisely the identical in numerous areas, though coverage names could fluctuate. This kind of protection gives a tax-free lump-sum cost to the policyholder’s household after they die. Coverage is available in completely different varieties, however usually falls into two classes:

Term life insurance coverage

This kind of coverage covers the insured for a set time period, paying out the dying profit if the policyholder dies inside a specified interval. This means funds may also be accessed within the years that the plan is lively. Once the time period expires, the insured can both renew or terminate the plan.

Permanent life insurance coverage

Unlike time period life insurance coverage, a everlasting coverage doesn’t expire. It can be known as complete of life coverage within the UK. In the US and Canada, protection is available in two most important sorts, every combining the dying profit with a financial savings element.

- Whole life insurance coverage: Offers protection for your complete lifetime of the insured and the financial savings can develop at a assured price.

- Universal life insurance coverage: Uses completely different premium buildings, with earnings primarily based on how the market performs.

A life insurance coverage coverage covers virtually all kinds of dying, together with these attributable to pure and unintentional causes, suicide, and murder. Most insurance policies, nonetheless, embody a suicide clause, which voids the protection if the policyholder commits suicide inside a particular interval, normally two years after the beginning of the coverage date.

Some life insurance coverage suppliers can also deny a declare if the policyholder dies whereas participating in a high-risk exercise equivalent to skydiving, paragliding, off-roading, and scuba diving. Additionally, an insurer could reject a declare primarily based on the circumstances surrounding the dying. For occasion, if the beneficiary is chargeable for or concerned within the policyholder’s dying.

Life insurance coverage policyholders are required to designate a beneficiary. This will be the insured’s partner, instant household, different kin, associates, enterprise companions, or perhaps a charitable group. Policyholders are additionally allowed to call a number of beneficiaries for his or her life insurance coverage and assign how a lot profit every individual or group will obtain.

There are two kinds of beneficiaries:

- Revocable beneficiary: They will be changed anytime with out the necessity for the policyholder to tell them.

- Irrevocable beneficiary: They can’t be changed until the policyholder secures a written permission signed by them.

Home insurance coverage, additionally known as owners’ insurance coverage within the US and Australia, just isn’t legally required in lots of international locations, though lenders set it as a situation for taking out a mortgage. Despite not being obligatory, many trade specialists nonetheless suggest property homeowners to take out protection given the massive monetary funding most individuals make when shopping for a house.

United States

According to Triple-I, an ordinary homeowners’ insurance coverage coverage within the US gives 4 important kinds of safety:

- Coverage for the construction of the house: Pays out for any bodily injury or loss to the home and different buildings throughout the property’s premises – together with sheds, garages, and fences – if this was attributable to a coated peril.

- Coverage for private belongings: Covers private possessions equivalent to clothes, electronics, furnishings, jewellery, and different home goods that had been broken or misplaced attributable to specified perils.

- Liability safety: Pays out for lawsuits and different authorized bills stemming from accidents to company whereas on the property or its premises.

- Additional dwelling bills: Covers the extra prices of dwelling away from dwelling – together with lodge payments, restaurant meals and different dwelling bills – if a home is inhabitable attributable to injury from an insured catastrophe.

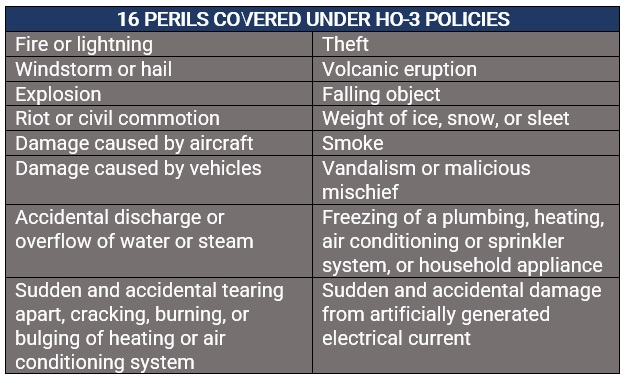

HO-3 insurance policies are the most well-liked kind of dwelling insurance coverage because it gives the widest protection. These insurance policies defend towards these 16 perils:

Other insurance coverage sorts accessible for US owners are:

- HO-1: The most elementary and restricted kind of coverage suited to single-family properties, though such a protection is extraordinarily uncommon these days

- HO-2: A slight improve from HO-1 insurance policies

- HO-4: Coverage designed particularly for renters, normally known as renters’ insurance coverage

- HO-5: The most complete type of owners’ protection

- HO-6: Coverage designed particularly for apartment homeowners

- HO-7: Coverage designed for a cellular or manufactured dwelling

- HO-8: A particular kind of householders’ coverage for older properties that don’t meet insurer requirements

Canada

Canadian property homeowners have three kinds of dwelling insurance coverage insurance policies to select from, every providing completely different ranges of safety.

- Standard protection: The most elementary type of safety, this covers solely the dangers or perils named within the coverage. Coverage usually consists of fireplace, lightning, smoke, and theft.

- Broad protection: Provides a wider vary of safety than customary insurance policies, however doesn’t provide full protection, in contrast to complete dwelling insurance coverage.

- Comprehensive protection: Also known as particular or all-perils coverage, this gives essentially the most intensive type of protection. It protects the property and its contents towards most kinds of dangers, apart from these particularly named as exclusions from the plan.

United Kingdom & Australia

Homeowners within the UK and Australia can entry two most important kinds of protection for his or her properties:

Buildings protection

Buildings insurance coverage covers the price to restore, rebuild, or substitute the construction of the house, together with its mounted fittings, whether it is broken by a man-made or pure catastrophe. This consists of fireplace, smoke, storm, flooding, falling objects, subsidence, or vandalism.

This sort of protection usually insures the house’s bodily construction – together with the partitions, ceiling, and roof – and everlasting fixtures – together with fitted kitchens, inner doorways, built-in home equipment, and toilet suites. Some insurance policies additionally cowl exterior buildings not hooked up to the home equivalent to garages, sheds, and fences.

Contents insurance coverage

Contents protection, in the meantime, pays out the price of changing private belongings inside the house if they’re stolen or broken. In the UK, protection is available in two most important sorts:

- Indemnity insurance policies: Pay out for the worth of an merchandise factoring in depreciation.

- New-for-old plans: Cover the price of changing an merchandise with a brand-new model.

Contents insurance coverage principally covers the next objects:

- Furniture – beds, eating chairs and tables, couch units, wardrobes

- Home accents – carpets, curtains, cushions, bedding

- Appliances – fridges and freezers, stoves and ovens, washing machines

- Kitchenware – cookware, cutlery, dinnerware

- Gadgets – laptops, cellular gadgets, TVs

- Clothing and trend equipment

- Toys, antiques, ornaments

- Garden tools – instruments, lawnmowers, backyard furnishings

One of the most important advantages of getting the appropriate insurance coverage kind is the peace of thoughts of understanding that if accidents and disasters strike, you might have the monetary means to rebuild your life. Having correct protection additionally implies that the street to restoration from sudden occasions is commonly sooner and smoother crusing.

What about you? What different insurance coverage sorts do you are feeling are important to guard your property? Share your ideas in our remark part beneath.

[ad_2]